Dollar Dominance Could Erode Without a Clear Successor Currency

Condoleezza Rice

Condoleezza Rice John Cochrane

John Cochrane Valerie RameyKrishna Guha

Valerie RameyKrishna Guha Sebastian Edwards

Sebastian Edwards Matt Klein

Matt Klein Stephen Redding

Stephen Redding John Hurley

John Hurley Arvind KrishnamurthyDavid Beckworth

Arvind KrishnamurthyDavid Beckworth Kenneth Rogoff

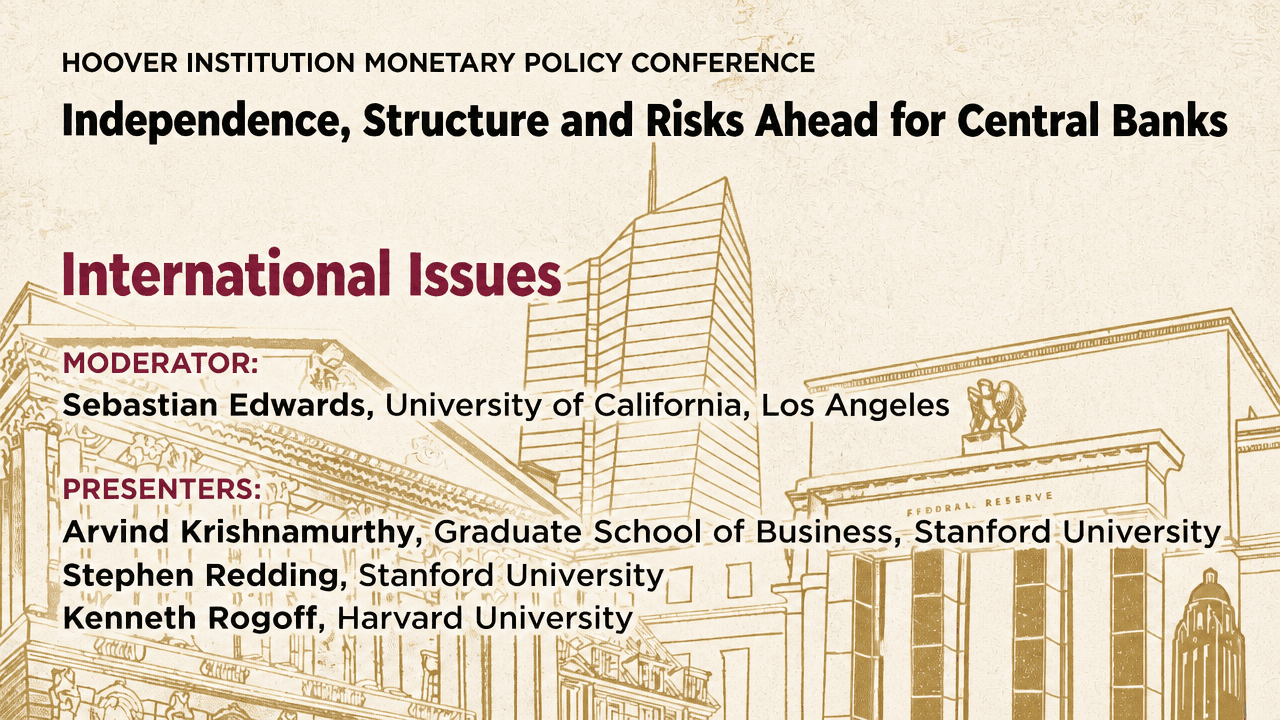

Kenneth Rogoff Jim BullardHoover InstitutionMonday, June 1, 202621 min read

Jim BullardHoover InstitutionMonday, June 1, 202621 min readAt a Hoover Institution conference on central-bank independence and international risks, Condoleezza Rice, Arvind Krishnamurthy, Stephen Redding and Kenneth Rogoff argued that dollar dominance can no longer be analyzed apart from U.S. security commitments, fiscal policy, technology competition and trade frictions. The central claim running through the discussion was that the United States still benefits from a powerful reserve-currency position, but that privilege depends on confidence in safe dollar assets and stable institutions. Krishnamurthy quantified the reserve-currency asset as a large interest-rate benefit, while Redding and Rogoff warned that tariffs, fiscal strain and political pressure on the Federal Reserve could make erosion costly even without a clear successor to the dollar.

The reserve-currency question is no longer separable from security, technology, and fiscal risk

Condoleezza Rice described the international problem as a transition away from the postwar order the United States and its allies built after World War II. The system’s distinctive feature, in her telling, was not only that it was American-led, but that it was deliberately non-zero-sum: a victorious power rebuilt former enemies, Germany and Japan, and brought both friends and foes into a trading order in which resources could be bought rather than fought over.

That system was also protected by American security commitments. NATO’s “attack upon one is an attack upon all,” the defense of Japan and South Korea, and the defense of sea lanes were all part of the same structure. Rice used what she emphasized was “a metaphor, not an analogy”: the United States as the sun, with other economies pulled into orbit by the gravitational force of its economy, the dollar, innovation, military power, and rules-based system.

The metaphor matters because Rice’s claim was that the gravitational field is shifting. During the Cold War, she argued, the national-security economy and the international economy could run on largely parallel tracks because the Soviet Union was a military giant but “an economic and technological midget.” No more than 4% of Soviet GDP, she said, was accounted for by international trade, mostly resources, and the Soviet economy was partly self-isolating.

China’s entry into the international system changed that separation. Rice dated the sharper break to roughly 2015, when Xi Jinping, in her words, “laid down the gauntlet” that China would surpass the United States in frontier technologies such as AI and quantum. The same period brought more visible conflict over the South China Sea and Taiwan, and China emerged as an economic, technological, and military peer competitor. The CEO narrative of efficient supply chains, high returns on investment, and favorable production conditions collided with a national-security narrative.

Her conclusion was not that international economics should be replaced by security analysis. It was that the issues now have to be analyzed together. Technology, national security, and the international economy are, for Rice, one conversation. She pointed to that day’s Wall Street Journal headlines about Anthropic and Mythos as an example of a technological development that, in her view, could drive productivity and economic growth while also carrying national-security implications.

There can't be a world in which the United States, which is its size and power and gravitational pull, is also the greatest source of uncertainty.

The uncertainty she identified was not only external. Rice said the “sun” is moving, sometimes with “a tweet on Truth Social,” leaving other countries unsure how to arrange themselves around American power. The Hoover Institution, she said, is trying to look beyond the current moment through work on what George Shultz called the “global economic and security commons.” The premise was that the United States cannot remain the anchor of a global order if it is also the main source of volatility in that order.

The hidden asset in dollar dominance is mostly an interest-rate asset, not an exchange-rate asset

The dollar’s reserve role can be treated as an asset with a measurable income stream. Arvind Krishnamurthy put the idea simply: the United States exports “safe dollar debt” in the way Taiwan exports semiconductors. The rest of the world wants dollar safe assets for reserves, collateral, liquidity, transaction services, and private banking-system uses. That demand lets the United States issue debt at lower yields than comparable alternatives.

The exercise was deliberately stark: suppose the rest of the world no longer wants safe dollar debt. What would happen to asset prices if the dollar ceased to be the world’s reserve currency?

Krishnamurthy chose 2016 as the baseline because he regarded it as a moment before the visible cracks of the last decade had developed very far. In the 2016 flow-of-funds data he used, Treasury and agency bonds equaled 94% of GDP, while private safe dollar bonds — corporate bonds, bank debt, deposits, and related instruments — equaled 111% of GDP. Foreign investors owned 39% of the public safe-bond share and 14% of the private share. In round terms, the United States had exported safe bonds worth about 45% of GDP.

| Measure | Krishnamurthy's 2016 baseline |

|---|---|

| Public safe dollar bonds | 94% of GDP |

| Private safe dollar bonds | 111% of GDP |

| Foreign-owned public safe bonds | 39% of public share |

| Foreign-owned private safe bonds | 14% of private share |

| Safe bonds exported by the U.S. | About 45% of GDP |

The second input was the convenience yield. Safe dollar debt, he said, has historically carried lower yields than benchmark alternatives. Work with Annette Vissing-Jørgensen put the convenience yield on Treasuries relative to corporate bonds at roughly 75 basis points over a long historical sample. More recent repo spreads suggested something closer to 90 basis points for some domestic safe-asset comparisons. For the international comparison — safe dollar assets relative to non-dollar assets, after accounting for exchange-rate risk — work with Hanno Lustig and Wenhao Jiang put the number around 2%.

Krishnamurthy used 2% for the calculation. If a reader preferred 1%, he said, they could halve the results.

The mechanism has two parts. First, if the United States no longer exports liquidity services, the trade balance has to adjust by the value of the lost services. That adjustment comes through the exchange rate: the dollar depreciates enough to change imports and exports. Second, if foreign investors no longer hold roughly 45% of GDP in U.S. safe assets, the domestic bond market has to absorb the supply. That requires higher U.S. interest rates.

Using a long-run trade elasticity of 0.3 and a bond-demand elasticity from his work with Vissing-Jørgensen, the calibration produced an exchange-rate depreciation of 8.81% and a rise in the U.S. safe interest rate of about 87 basis points. Krishnamurthy stressed that the exchange-rate effect is modest because the calculation compares steady states rather than one-day market reactions to announcements, tariffs, or wars.

The more consequential number was the present value of the lost seigniorage. With 45% of GDP in foreign holdings of dollar bonds and a 2% convenience yield, the annual seigniorage value is about 1.05% of GDP. Discounting that stream as a risky asset growing with GDP gave a present value of about $33 trillion.

| Input or result | Value | Meaning in Krishnamurthy's calculation |

|---|---|---|

| Seigniorage base | 45% of GDP | Foreign holdings of dollar bonds |

| Convenience yield | 2% | Yield discount on safe dollar assets |

| Annual seigniorage loss | 1.05% of GDP | Income stream lost if reserve-currency demand fully erodes |

| Present value | $33 trillion | Estimated value of the reserve-currency asset |

Krishnamurthy described this as a “hidden asset” distributed across the U.S. financial system. Banks benefit from being able to issue dollar deposits for which there is ample global demand. Housing values reflect mortgage finance tied to convenience yields on safe collateral. Government debt benefits through lower debt-service costs, which affect the future tax burden on U.S. households.

His summary was blunt: the United States’ “exorbitant privilege” has appreciated the dollar, but only modestly. Its larger effect is on borrowing costs and asset values. A world in which the dollar is no longer the reserve currency is, in this model, less an exchange-rate catastrophe than a repricing of the U.S. balance sheet. The calibration compared a 2016 baseline with a full convenience-loss case in which debt held abroad falls from 45% of GDP to zero, seigniorage falls from 1.05% of GDP to zero, and the government dollar interest rate rises from 0.53% to 1.40%.

The calculation did not assume that loss of reserve status was imminent. Krishnamurthy said he sees cracks, but also complementarities that still hold the dollar system together. His warning was about the size of the asset before the United States “choose[s] to give it away.”

Tariffs have remade sourcing patterns more than they have fixed the trade deficit or inflation

The trade-policy break is sharper in sourcing patterns than in the trade deficit or the inflation rate. Stephen Redding began from the postwar baseline: for much of the period after World War II, tariffs appeared largely settled in advanced economies. Multilateral and regional liberalization under GATT and the WTO reduced the average import-weighted U.S. tariff to less than 2% by the mid-2010s.

That changed in 2018–2019 and again in 2025–2026. Redding said the United States imposed tariff waves that initially raised protection close to levels last seen during the Smoot-Hawley tariffs of the 1930s. He also said, in describing the current policy setting, that some tariffs had been struck down — the IEEPA tariffs by the Supreme Court and, as he put it, the Section 122 tariffs by the International Court of Trade the previous day — while the administration was planning new tariffs under other legal justifications. The trade-policy shift sat alongside broader geopolitical stress: Russia-Ukraine, China-U.S. confrontation, and conflict in the Middle East.

His data showed a long postwar decline in the effective applied U.S. tariff, followed by a sudden spike in 2025–2026. Imports as a share of GDP rose as tariffs came down, and that aggregate rise, he argued, may understate globalization because of the growth of global value chains. Tariff revenues as a share of GDP rose only modestly with the recent tariff wave.

Foreign retaliation was more limited than standard trade models might suggest, with China the major exception. China imposed tariffs aggressively on U.S. goods, while the rest of the world responded more mutedly, possibly for geopolitical reasons.

One distinctive feature of the new tariff period is the gap between statutory and applied tariffs. Redding attributed it to imperfect enforcement, exemptions, and a sharp increase in compliance with USMCA rules of origin. Before the 2025–2026 tariffs, only about 45% of trade within the USMCA area complied with rules of origin needed to qualify for duty-free treatment. After tariffs rose, compliance increased to more than 85%. When tariffs were low, the fixed costs of compliance often were not worth paying. When tariffs became high, firms paid those costs to escape duties.

That adjustment is a central part of the argument: tariffs do not simply raise a wall and leave commerce unchanged behind it. They induce reorganization, avoidance, compliance spending, and rerouting. Some trade becomes duty-free, but not costlessly.

The most visible reorganization is the “great reallocation” of U.S. import sourcing. China’s direct share of U.S. imports peaked above 20% around 2015 and had fallen to around 11%, roughly its share before China joined the WTO. Mexico, Vietnam, Taiwan, and other Asian suppliers moved up the ranking of U.S. import partners. Redding described the pattern among the top 20 import partners as a reshuffling rather than a wholesale diversification away from a concentrated set of suppliers.

The direct China share can also mislead. The United States remains indirectly exposed to China through inputs embedded in goods imported from Vietnam, Taiwan, Cambodia, and other countries. The reallocation therefore changes the map of direct sourcing, but not necessarily the underlying exposure to Chinese intermediate goods.

Redding was clear that this reshuffling has a resource cost: “There was a reason why we weren’t importing this material from these countries before.” The change reflects policy pressure, not a free efficiency gain.

On the trade deficit, his conclusion was conventional but important. The U.S. trade imbalance as a share of GDP remained broadly flat despite large changes in trade policy. That was not surprising, he said, because the trade deficit is driven by expenditure relative to income, or saving relative to investment. Tariffs reduce both imports and exports. Their net effect on the trade deficit is therefore modest and subtle.

On inflation, Redding distinguished price-level effects from sustained inflation. Tariffs affect the level of prices; they do not permanently affect the rate of price growth. Estimates he cited from Alberto Cavallo and colleagues put the cumulative 2025–2026 tariff impact on the CPI at about 0.8 percentage points. Redding said that was roughly what a simple calculation would imply: an applied tariff increase of about 8% multiplied by imports at about 11% of U.S. GDP gives just under 1 percentage point.

Most of the burden, in his reading of the evidence, has fallen on U.S. consumers, importers, and retailers rather than foreign exporters. There was relatively little evidence of a large-scale fall in prices received by foreign exporters. Some U.S. wholesalers and retailers absorbed part of the price increase in margins, helping keep the measured CPI effect modest.

Looking ahead, Redding placed tariffs below other immediate forces for U.S. consumer prices. The dollar exchange rate may matter as much as the tariffs; oil may matter more. He pointed to a sharp rise in Brent prices following what he called “the Iran war” and said forecasters estimate that oil at $130 to $140 per barrel could add roughly 0.75 percentage points to the CPI level. As with tariffs, the direct oil effect is a level effect, but it becomes more dangerous if it shifts wage-setters’ and firms’ inflation expectations.

His trade-policy conclusion was not that tariffs are irrelevant. It was that they are more consequential for sourcing patterns, uncertainty, and welfare than for eliminating trade deficits or generating persistent inflation. Trade, in the neoclassical view he invoked, operates like an improvement in production technology: it lets an economy obtain goods without producing everything itself. It creates aggregate gains and domestic winners and losers. Tariffs reduce access to those gains, and the recent U.S. experience shows the costs through reallocation and higher domestic prices, even if the aggregate CPI effect remains limited.

Dollar dominance brings tools and obligations that seigniorage alone does not capture

The dollar’s role carries advantages and costs that are harder to model than a convenience-yield stream. Kenneth Rogoff accepted the importance of Krishnamurthy’s calculation but added sanctions, information, and institutional leverage on one side; insurance-like losses and military costs on the other.

The sanctions channel was central. Rogoff said one advantage of being the dominant currency is the ability to use sanctions, whether or not one thinks they are always effective. That tool was used intensely before the current presidency. A related advantage is information: because so many transactions touch the dollar, the United States gains visibility into what others are doing. Rogoff said Europeans dislike that almost as much as the Chinese do. He also included swap lines as another form of potential leverage or weaponization.

On the cost side, Rogoff cited what Hélène Rey and Pierre-Olivier Gourinchas call “exorbitant duty.” If the dollar is treated as a safe asset and appreciates in bad global states, the United States provides insurance to the rest of the world: U.S. foreign holdings lose value while foreign holders of U.S. assets gain. That cost can be quantified, he said, and had been studied as early as Walter Salant’s 1964 QJE paper.

The larger cost, in Rogoff’s view, is military. “You can’t be even in the game of having a major currency, much less being a dominant currency, without having a military,” he said. The point was not only the protection of assets. U.S. military dominance gives the country leverage in making and enforcing the rules of the global system: how SWIFT works, how the IMF works, and how financial infrastructure is organized. He emphasized that this is not unique to President Trump; Nixon, Reagan, Lyndon Johnson, and others also used U.S. leverage.

Rogoff agreed that 2015 is a plausible peak year for dollar dominance. He referred to work with Carmen Reinhart and Ethan Ilzetzki measuring dollar dominance in the global exchange-rate system, and said his book updates that measure and shows some decline. In his view, erosion of dollar dominance preceded Trump, but current policy has aggravated the situation.

He linked trade policy to financial dominance through general equilibrium. Frictions in trade filter into finance. If the United States gains heavily from international finance, then restrictions on trade can damage those gains. The point was not only a criticism of Trump. Rogoff said skepticism of trade also appears among progressives, citing Bernie Sanders.

The deepest vulnerability, for Rogoff, is fiscal. He criticized the 2010s academic confidence that debt no longer mattered because interest rates were low and expected to remain low. The United States, he said, is the world’s largest debtor; the federal government has approximately more debt than all other advanced countries put together, and the picture is even larger if corporate debt is included. If global real interest rates rise because of populism, high debt levels, military spending, or other forces, the United States becomes more vulnerable.

He was skeptical that AI will lower the neutral real interest rate. The Federal Reserve can set inflation over the long run, he argued; the relevant question is what AI does to the real interest rate. Like most positive productivity shocks, if AI is one, he expects it to push the real interest rate up through standard channels, unless one builds a more creative model to get the opposite result.

That matters for central-bank independence because certain shocks create pressure on the central bank in a way others do not. A pandemic or global financial crisis can make fiscal and monetary expansion point in the same direction. A war-like shock, cyberwar, or major military conflict can push interest rates up holding other policies equal. That kind of shock makes fiscal dominance and political pressure on monetary policy more acute.

Rogoff was dismissive of stablecoins as a rescue for dollar dominance. He agreed with Barry’s earlier view, as he reported it, that stablecoins are “almost a non sequitur” as a strategy for making the dollar more popular. He said the GENIUS Act might help the dollar the way printing $10,000 bills might have helped the dollar: perhaps useful for demand, but potentially costly to the Treasury relative to the savings.

AI, in Rogoff’s account, is powerful but indeterminate. Its potential is tremendous, but so are possible job losses and military costs. He did not try to resolve the balance in the time available.

Dollar decline does not require a clean successor currency

The main objection to dollar-decline arguments is that they have sounded plausible before and still proved premature. Sebastian Edwards recalled earlier Stanford discussions, associated with Ron McKinnon, in which the yen was expected to replace the dollar. Decades later, the dollar remained the reserve currency. If the dollar loses its role now, Edwards asked, what replaces it? The Swiss franc, euro, and yuan each have obvious limitations in his framing. Without a replacement candidate, the world may be stuck with the dollar for a long time.

Rogoff rejected the replacement framing. The relevant risk, he said, is not that another currency cleanly replaces the dollar, but that the United States becomes destabilized through fiscal dominance or political dominance over the Federal Reserve. The better historical comparison is the 1970s, when no rival currency had to replace the dollar for the system to become unstable. Over short periods, he said, nothing dramatic needs to happen. The dollar can lose market share gradually. China will take share because it wants strategic autonomy around Taiwan and the South China Sea and expects possible financial sanctions. Europeans, too, may seek alternatives. But if U.S. policy remains sound, the shift can be smooth and mild. If the United States has internal problems, bonds and dollar assets can lose share without a single successor.

Redding made a similar point from the transaction-cost side. Maybe nothing replaces the dollar. The world could become more fragmented and less costless, with higher transaction costs instead of a new single dominant currency. The network benefits of one dominant currency are large, but instability in the United States could still reduce the dollar’s ability to serve that function.

Krishnamurthy accepted “erosion and muddling around” as a possible path. But he emphasized the incentive: a $33 trillion prize is large enough for economies to search for ways to claim it, even if it is not claimed in five or ten years.

Three disputes then mattered more than the hunt for a single successor: whether there is evidence of erosion, whether Treasuries remain stapled to the dollar’s reserve role, and whether dollar-denominated assets can be supplied outside the United States without preserving the same privilege for the U.S. balance sheet.

On evidence, Krishnamurthy’s answer was cumulative rather than dispositive. No single data point, in his view, settles the question. He looks across quantities, asset prices, and covariances, all of which he said point in one direction. He acknowledged that many measures are likely mismeasured. But the covariance shift matters: after the tariff shock the previous year, the dollar depreciated, whereas in previous episodes of uncertainty there had typically been a flight to the dollar. Convenience yields have fallen. Quantities are harder to pin down. Collectively, he said, the evidence indicates erosion, though not enough to measure precisely how far it has gone.

That answer did not satisfy every concern raised from the floor. John Hurley said he had struggled to find evidence of de-dollarization in the data: global FX reserve holdings of dollars were lower in the 1990s than now, the yuan’s share had declined recently, and gains seemed concentrated in small shares for currencies such as the Australian, Canadian, and New Zealand dollars. David Beckworth pointed to arguments that some apparent decline in China’s dollar holdings may reflect custodial shifts rather than true selling, while China’s large surpluses may still require acquiring dollar assets. The panel did not resolve those measurement questions into a single indicator.

On satiation, Krishnamurthy said the answer is more complicated than simply “the United States issued too many Treasuries.” Echoing Hanno Lustig’s earlier comments, he said long-term Treasuries no longer look like convenience assets in the same way. T-bills and repo still do. The market has bifurcated: the world treats only part of the Treasury complex as safe dollar assets — “the part that I’m fairly sure you’re going to pay back in the next three months.”

That bifurcation also bears on whether Treasuries are stapled to the dollar. Krishnamurthy said many factors drive dollar dominance, including military and institutional power. But across the historical literature, the provision of a safe and liquid asset is consistently important in centering a currency. In that sense, Treasuries are stapled to the dollar. If parts of the Treasury market look less liquid or less safe, that can weaken the staple.

John Cochrane challenged the assumption that reserve use of dollars requires large holdings of U.S.-issued securities. A transaction can be denominated in dollars without holding many dollars, and non-U.S. entities — for example, a German company — can issue dollar-denominated bonds. Krishnamurthy replied that foreign issuers of dollar assets do so against non-dollar revenues and therefore run currency mismatch at a cost. The United States issues dollar liabilities against dollar revenues; it “sort of get[s] it for free.” That asymmetry is built into his computation.

Matt Klein pushed on whether the convenience yield might already be negative, citing disagreement among the panelists and earlier speakers. Krishnamurthy distinguished absolute from relative convenience yields. Comparing bunds with Treasuries is a relative exercise. His seigniorage calculation requires the absolute convenience yield on safe dollar assets: the value of liquidity services exported by issuing those assets. That absolute measure, not a cross-currency spread alone, enters the computation.

Dollar erosion, on this account, may show up first in prices and covariances rather than headline reserve shares. It may also be obscured by custodial shifts, portfolio substitutions, and private dollar creation outside the United States. The panel left the measurement problem open, but narrowed the conceptual one: decline does not have to mean replacement; it can mean fragmentation, thinner convenience yields, higher transaction costs, and a weaker Treasury-dollar link.

The dollar-as-burden argument did not explain manufacturing decline

John Cochrane put forward a view he said he did not hold but wanted the panel to address: that the dollar has been a burden to the United States. In this account, America imported goods, consumed them, and sent foreigners pieces of paper, hollowing out manufacturing; losing reserve-currency privilege would be a day to celebrate because Americans could return to producing goods and putting them on boats. He compared the argument to Spain and Portugal in the 16th century, when gold from the Americas financed consumption and coincided with productive decline.

Redding and Rogoff both rejected the argument as an explanation for manufacturing decline. Redding’s answer was that trade in assets can generate gains just as trade in goods can. If the United States provides safe assets, secure property rights, and an attractive investment environment, then foreign investment in the United States and a corresponding trade deficit can be a source of gains from international exchange.

He also judged the dollar-burden channel to be modest relative to technology in explaining manufacturing employment. A long historical comparison with agriculture makes the point: 60% of Americans once worked in agriculture, and most no longer do, mainly because of technology rather than trade. Redding applied the same logic to manufacturing. The China shock hurt particular communities and regions intensely, but at the economy-wide level, the decline in manufacturing employment was likely driven more by long-run technological change than by trade or the dollar’s reserve role.

Rogoff agreed. Krishnamurthy’s magnitude for the reserve-currency benefit seemed plausible to him, but it likely had very little to do with manufacturing hollowing out. Automation, not the reserve currency, was the main explanation. Rogoff said the China shock paper had been politically attractive and repeatedly invoked, but he viewed its aggregate quantitative importance as small relative to other forces.

The related question of tariff revenue produced a different kind of objection to the free-trade baseline. Jim Bullard asked why tariffs should not be treated as one tax instrument among many. If other taxes, especially capital taxes, are distortionary, perhaps revenue from trade taxes could reduce reliance on more damaging forms of taxation.

Redding gave three reasons trade economists typically see tariffs as a costly tax instrument. First, even though the tariff is levied on imports, domestic producers of similar goods raise prices too. The tariff therefore operates as both a consumption tax and a production subsidy. Trade economists call the production-subsidy element a byproduct distortion: the tariff taxes consumers while also subsidizing domestic production.

Second, the tax base is small. Imports are about 11% of U.S. GDP. A consumption tax can apply to a much larger base. Because distortions rise with the square of the tax rate — the Harberger triangle logic — raising a given amount of revenue from a smaller base requires higher rates and larger distortions.

Third, while one can make a case for some tariff in an optimal tax system, Redding said trade economists would generally expect it to be small relative to other available instruments. He acknowledged that a consumption tax is regressive, but also noted that in an AI world where more returns may go to capital rather than labor, taxing sales has some attractions as an alternative to capital taxation.

Edwards’s question about AI exports pulled the same issue into services. In emerging markets, he said, many people subscribe to Anthropic and ChatGPT, and exports of large language models could become “absolutely astonishing.” Redding treated the question as part of a broader rise in trade in services. Digital services could become a major source of gains and a trade-policy issue. He pointed to debates in Europe over whether digital goods should be taxed in response to U.S. tariffs. A larger unresolved question is whether digital trade and services can substitute for some goods trade or complement it. He presented that as an open research agenda rather than a settled conclusion.