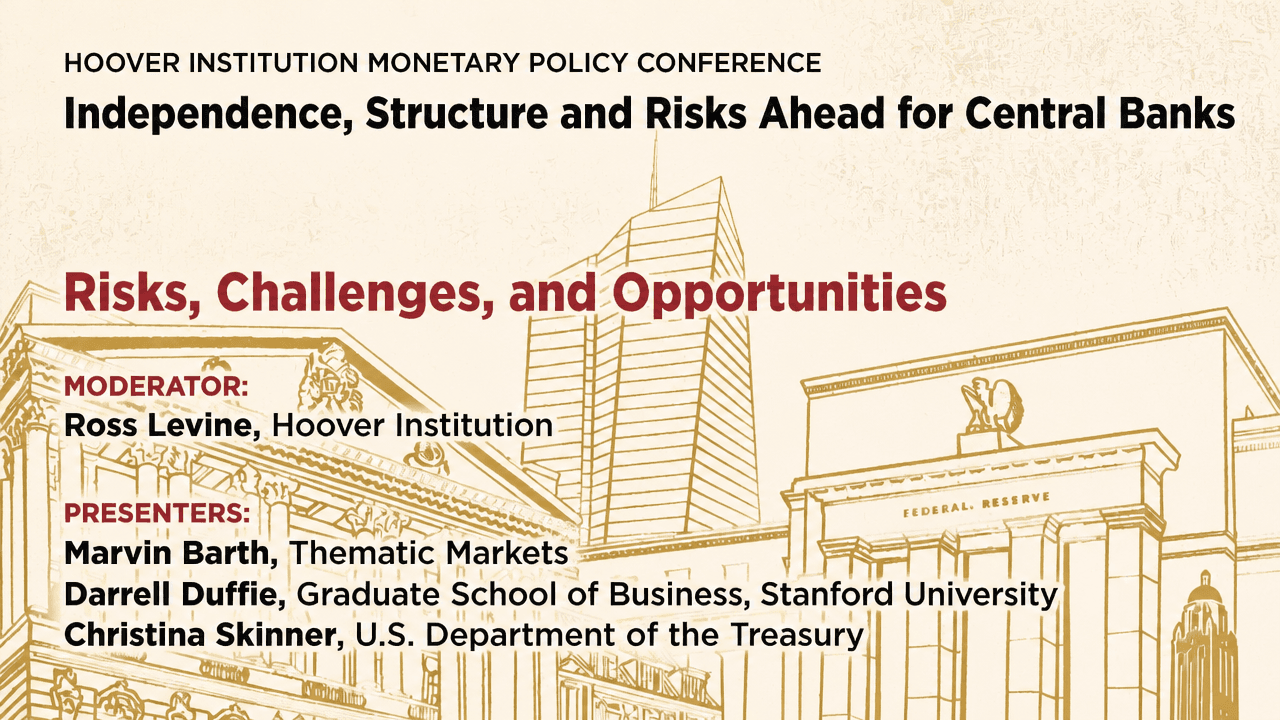

Central Banks Face Accountability Tests Across Independence, Reserves, and Stability Policy

Ross Levine

Ross Levine Michael Bordo

Michael Bordo Yuriy Gorodnichenko

Yuriy Gorodnichenko Darrell Duffie

Darrell Duffie Bill Nelson

Bill Nelson Marvin Barth

Marvin Barth Steven Davis

Steven Davis Mickey LevyChristina SkinnerHoover InstitutionMonday, June 1, 202619 min read

Mickey LevyChristina SkinnerHoover InstitutionMonday, June 1, 202619 min readAt a Hoover Institution conference on central-bank independence, Marvin Barth, Darrell Duffie and Christina Skinner each framed the next phase of monetary and financial policy as an accountability problem. Barth argued that the Federal Reserve’s policy failures and lack of humility have weakened its political legitimacy; Duffie said shrinking the Fed’s balance sheet depends on changing reserve demand and payment mechanics, not simply selling assets; and Skinner argued that financial stability policy should weigh growth and economic security rather than treating every visible risk reduction as a net gain.

Accountability is the constraint running through independence, plumbing, and stability policy

The central problem was not whether public institutions should eliminate risk. None of the three presenters treated that as possible, and Christina Skinner explicitly argued that trying to do so can make the system more brittle. The harder question was how institutions with delegated authority remain accountable when they decide which risks to tolerate, which markets to constrain, and which failures to absorb.

Marvin Barth put the problem in democratic terms. Federal Reserve independence, in his view, is politically fragile because the Fed has combined policy failure with insufficient humility toward the citizens who bear the costs. Darrell Duffie put the same issue in operational terms: if the Fed wants a smaller balance sheet, it cannot simply sell assets and hope money markets absorb the shock; it has to confront the liabilities, payment mechanics, and liquidity rules that create demand for trillions of dollars of reserves. Skinner put it in regulatory terms: financial stability policy should not become a one-way ratchet toward precaution, because suppressing all visible risk can also suppress growth, adaptation, and resilience.

Those are different domains, but the institutional tension is the same. Independence without accountability becomes politically vulnerable. Balance-sheet discipline without operational redesign becomes market fragility. Macroprudential caution without prioritization becomes a drag on the real economy. The panel did not resolve those tensions into a single policy program. It made them explicit.

The Fed’s legitimacy problem, Barth argues, is partly self-created

Marvin Barth treated the current threat to Federal Reserve independence as a risk the institution helped create. He said he did not condone attacks on Fed officials, but he sympathized with Americans frustrated by “the lack of accountability for an institution that has failed badly in its mission and is desperately in need of reform.” The challenge he put to the room was not whether central-bank independence is necessary; he accepted that premise. The challenge was how to make an independent central bank accountable.

While I do not condone the methods employed against Fed officials, I sympathize with many Americans' frustration at the lack of accountability for an institution that has failed badly in its mission and is desperately in need of reform.

Barth’s indictment of the Fed came through a broader forecasting framework built around four forces: localization, “being is believing,” global entropy, and the politics of rage. His claim was that these forces have raised U.S. potential growth, the marginal product of capital, inflation pressures, and demand for decentralization in finance, while shortening or shrinking globalized manufacturing supply chains.

Localization, in his account, began around an “unheralded but important breakpoint” in 2012. Cross-border investment that had long moved from rich economies toward poorer ones reversed direction. In the United States, he said, that coincided with the largest postwar investment boom on a cumulative basis. At the same time, the import share of U.S. GDP peaked after five decades of increases and began to fall. Barth’s explanation was technological: when automation becomes cheaper than outsourced labor, firms have more reason to locate production closer to high-value customers. “One could say,” he said, “that globalization is the first casualty of AI.”

The inflation component was more directly aimed at the Fed’s analytical framework. “Being is believing” was Barth’s phrase for self-fulfilling expectations. He accepted the standard proposition that when consumers believe inflation is rising, they are more willing to accept higher prices. But because inflation expectations were stable for many years, he argued, econometric models often neglected or minimized them, and that seemed to work. Before COVID, he said, expert forecasts and model-based approaches outperformed consumer-expectations measures.

After COVID, Barth argued, the relationship reversed. He said the Fed’s flexible average inflation targeting “successfully unhinged inflation expectations,” adding that, in his view, this was the framework’s intent. The point was not merely that consumers forecast inflation better than experts. It was that people closest to prices helped create inflation persistence through their expectations and reactions. He said the stronger predictive signals appeared in reverse order of education, a pattern he suggested likely corresponded to institutional trust.

That analytical failure became a political failure. Barth said bond traders and professional economists repeatedly failed to predict de-anchoring of expectations from the 1970s through COVID. Treating market inflation pricing as representative of consumer price expectations, he argued, reflected “a profound ignorance of finance, economic history, and theory.” Consumers who form prices, he said, struggle to balance budgets — “and by the way, they vote.”

You are not going to educate populism away.

The politics of rage, for Barth, is not mainly an education story. In a report he wrote a decade earlier, he said, he found that the primary driver of populism was average citizens’ perception that elites had disenfranchised them while pursuing their own interests. Citing David Shor, he said trust mattered more than education in predicting Trump support. Citing anthropologist Heidi Larson, he said perceived loss of control, rather than ignorance, was central to vaccine hesitancy and conspiracy theories.

For the Fed, the warning was blunt: voters do not trust elites to act in their best interests, and after repeated expert and policy failures whose costs fell on average citizens, Barth asked, “who can blame them?” He situated American populism in a longer Jacksonian tradition, emphasizing hostility toward centralized finance and national banking. Andrew Jackson, he noted, killed the Second Bank of the United States. The Fed’s vulnerability, in Barth’s telling, should be read partly through that tradition.

His global “entropy” theme carried the same logic into geopolitics and supply chains. Barth said the postwar liberal order began collapsing roughly three decades ago, and he argued that the West forgot that power depends on manufacturing guns, 155-millimeter artillery shells, and drones — not on GDP alone. China, he said, did not make that mistake. In his view, Chinese overcapacity is not an economic bug but an intentional geoeconomic strategy: a way to climb the technology frontier, build military-industrial capacity, and weaken competitors’ industrial capacity and technological leadership. He connected that strategy to Unrestricted Warfare, a 1997 book by two People’s Liberation Army senior colonels.

Barth said his own research shows Chinese import penetration at the three-digit industry level directly reducing total factor productivity in U.S. manufacturing firms by undermining learning-by-doing as firms are pushed out of business or into runoff mode. He stressed that he was not attributing this to superior Chinese factory efficiency; he said Chinese total factor productivity growth has been negative for more than a decade.

The macroeconomic implication, in Barth’s account, is that redundancy, resilience, defense demand, resource nationalism, transport costs, and supply-chain security are changing the inflation and growth environment. Localization, he said, is raising potential growth, the marginal product of capital, and neutral interest rates while compressing imports. Inflation expectations are producing persistence. Global entropy is increasing demand for redundancy and defense while raising costs. The politics of rage is pushing for institutional accountability, deregulation, and decentralized finance.

His tariff example was meant to show why standard models miss the shift. Generic tariff studies, Barth said, would have predicted that broad U.S. tariff increases would reduce capital expenditure and impair productivity. He argued that many such studies are based on small developing economies rather than a large, mostly closed economy at the technological frontier. Barth forecast the opposite: tariff walls would accelerate localization-driven capex and protect U.S. manufacturing from what he called productivity-killing Chinese subsidies.

His slide showed the United States attracting $2.578 trillion of announced investments in 2025, or 79 percent of the listed global total; including “full Stargate,” it showed $2.978 trillion, or 81 percent. The same slide attributed $1.368 trillion to U.S. manufacturing and $1.656 trillion to announcements after “Liberation Day.” Barth summarized the evidence as roughly 80 percent of announced global capex, with about two-thirds occurring after “Liberation Day,” and more than half in manufacturing. He said hard data on capex and durable-goods orders validated the announcements, while adding that it was too early to claim victory on productivity.

The Fed, Barth argued, has been reading the same economy badly. Despite nearly 500 economists, he said, actual U.S. GDP growth has outpaced the most optimistic FOMC member estimate of trend growth for more than a decade. Realized real interest rates, he argued, have also made a mockery of FOMC neutral-rate estimates. When the Fed describes policy as restrictive, Barth invoked The Princess Bride: “I do not think it means what you think it means.”

He rejected the idea that COVID-era shocks excuse the record. Warren Harding, he said, faced World War I, the Russian Revolution’s disruptions of grain and oil prices, a major steel strike, and the Spanish Flu while constrained by the gold standard. Arthur Burns faced the dollar float, Nixon’s price controls, the Arab oil embargo, and the “Great Grain Robbery,” without modern inflation-expectations data or an accepted understanding that the Phillips Curve can shift.

By Barth’s measure, the Powell Fed was the seventh-worst in history on inflation and the fourth-worst of the fiat era. He said that comparison was unfair to Paul Volcker, because Volcker inherited 12 percent inflation. Powell, by contrast, inherited sub-2 percent inflation and, Barth said, was “bequeathing Kevin Warsh 4.4% PCE inflation that’s accelerating.” He also emphasized that the record was not Powell’s alone: in his view, the poor performance was a “team effort,” with the Powell Fed having the lowest dissent rate since the Fed-Treasury Accord secured independence.

Barth closed with Themistocles. Athens’ hero saved Greece from conquest, but was later ostracized by public vote amid charges Barth said historians regard as questionable and factional. Yet historians also agree, he said, that Themistocles lacked humility before his fellow citizens. Barth’s warning to the Fed was that a democracy can turn even on heroes. The current political assault on the Fed, he argued, involves factionalism, but also follows “objective policy failures the Fed continues to deny.”

The balance-sheet constraint is on the liability side

Darrell Duffie redirected the Fed balance-sheet debate away from asset purchases. Discussions of Fed independence often focus on whether the Fed bought too many assets, he said, including concerns raised by Kevin Warsh in a Group of Thirty speech around the IMF meetings. Duffie’s point was that this is not where the immediate constraint lies. The balance sheet is kept large by liabilities, and those liabilities are why the Fed’s balance sheet remains above $6 trillion.

Currency accounts for about $2.5 trillion, which Duffie treated as essentially fixed for this purpose: the Fed is not going to “hoover up all the currency out there.” The Treasury General Account was about $0.9 trillion, and Duffie noted that the Treasury Borrowing Advisory Committee had recently discussed ways to reduce it, possibly by as much as half. Reverse repos accounted for about $0.3 trillion.

The adjustable liability is reserve balances: about $2.9 trillion in deposits that commercial banks hold at the Fed to run business operations and meet liquidity requirements. A materially smaller Fed balance sheet would therefore require lowering banks’ demand for reserves, not merely selling assets into the market.

| Federal Reserve liability | Amount described by Duffie |

|---|---|

| Reserve balances | $2.9T |

| Currency | $2.5T |

| Treasury General Account | $0.9T |

| Reverse repos | $0.3T |

| Other liabilities | Shown on slide, not specified in transcript |

The question Duffie posed was why banks needed $2.9 trillion in reserves in 2026 when $10 billion sufficed in 2007. His answer was liquidity regulation interacting with the payment system. After the financial crisis, Congress and regulators insisted that large banks be self-sufficient in liquidity. In practice, Duffie said, the largest banks came to avoid drawing on the Fed when they needed reserves to make payments. That means they need to begin each day with enough reserves to cover the payments they expect to make.

Duffie did not argue for returning to scarce reserves. He quoted Governor Chris Waller’s line that having banks “scrounge under the couch cushions” for money is “massively inefficient and stupid,” and said he agreed. The goal, if the Fed wants a smaller balance sheet, would be to reduce demand for reserves while still allowing banks to run payments and meet liquidity needs.

His four options were ordered by likely difficulty and impact.

| Policy | Duffie’s characterization |

|---|---|

| Offset reserve-supply shocks with open market operations | Least difficult; could smooth bumps but likely save only around $100 billion or $200 billion. |

| Encourage banks to obtain liquidity from the Fed when short | Could matter substantially if liquidity regulations no longer discourage use of Fed facilities or overdrafts. |

| Add a liquidity savings mechanism to Fedwire | Operationally difficult, but potentially able to reduce reserve needs significantly by offsetting payments. |

| Tier interest paid on reserves | Potentially the largest effect, but politically and practically difficult because banks would resist lost interest income. |

The easiest option would smooth temporary reserve shortages. If tax payments caused the Treasury General Account to rise and drained reserves from the banking system, the Fed could fill the pothole with temporary open market operations. Duffie attributed versions of this idea to Bill Nelson and Annette Vissing-Jorgensen. But he said the likely scale was modest — perhaps $100 billion or $200 billion — not a major reduction relative to $2.9 trillion.

The second option would change banks’ willingness to use Fed liquidity. If large banks believe intraday overdrafts, the discount window, or standing repo operations make them appear not self-sufficient, they will hold more reserves instead. Duffie used daylight overdrafts to show the change. Before the financial crisis, the largest banks used intraday overdrafts heavily, at times around $100 billion to $150 billion per day. Since the crisis, they have largely stopped. Most of the time, abundant reserves made overdrafts unnecessary. But in September 2019, when reserves became tight, Duffie said the largest banks still did not overdraft, and interest rates spiked because there were not enough reserves in the system.

The third option would make the payment system itself more efficient. Most developed-market central banks, Duffie said, have a liquidity savings mechanism; the Fed does not. The Bank of Japan, Bank of Canada, Bank of England, and European Central Bank all have systems that allow banks to make outgoing payments from incoming payments rather than requiring each bank to fund outgoing payments from its own reserve stack at the start of the day. Duffie said such systems can be effective, though adding one to Fedwire would require major operational work.

The fourth option would tier the interest rate paid on reserves. Under tiering, the Fed would pay the full administered rate only on reserves needed for a bank’s operations, and a lower rate on balances above that level. Banks would then try to avoid holding excess reserves merely to earn interest. Duffie cited New Zealand and Norway as examples where tiering reduced demand for reserves or revived interbank lending. He also noted that the Fed itself initially designed interest on reserves with two tiers in 2008, though that structure lasted only five or six weeks before both tiers were pushed to zero during the crisis.

Duffie’s practical warning was direct. If the Fed sold assets today and hoped for the best, he said, “it would be quite a mess” — worse than September 2019. Reserve balances were $1.4 trillion then; they were $2.9 trillion in his 2026 figures, yet he said the system remained constrained in similar ways. A smaller balance sheet requires redesigning reserve demand, payment operations, or reserve remuneration. It is not an asset-sales exercise alone.

FSOC’s risk framework is being pushed back toward growth and security

Christina Skinner spoke from the Treasury Department about financial stability policy rather than monetary policy. Under Secretary Bessent’s leadership, she said, the Financial Stability Oversight Council is trying to reorient its approach toward first principles: mitigate risk, but support rather than constrain a dynamic and resilient market economy.

FSOC was created by the Dodd-Frank Act in 2010 after the financial crisis. Skinner described its broad mandate as identifying risks to U.S. financial stability, responding to emerging threats, and promoting market discipline. Congress’s decision to put the Treasury Secretary at the head of the council was important, in her view, because financial stability policy involves tradeoffs: judgment under uncertainty, and the balance between public intervention and private risk-taking.

The statute left “financial stability” largely undefined. That ambiguity gave FSOC flexibility, but it also made the council’s direction dependent on the intellectual framework applied to the problem. In FSOC’s early years, Skinner said, the council emphasized designating nonbank financial firms for enhanced supervision, reflecting a view that systemic risk could be mitigated by extending bank-like regulation beyond banks. She called that view flawed. Later, she said, FSOC’s scope expanded toward broader and more speculative concerns, including climate-related financial risk, sometimes over long or undefined horizons.

Regulation also accumulated across the landscape. Skinner did not argue that every reform was unjustified; she said many were well-motivated and could be individually defended. Her criticism was that they were rarely assessed in terms of aggregate effects on market functioning, capital formation, or the economy’s capacity to grow. After 15 years of FSOC, she said, Treasury concluded it was necessary to reconsider not the goal of financial stability policy, but the framework through which that goal was pursued.

The first-principles question was what financial stability policy is for. In a market economy, Skinner said, the objective cannot be to eliminate all risk. Risk is inseparable from innovation, investment, and growth. Macroprudential policy should instead prevent financial disruptions from propagating in ways that materially impair the real economy — business formation, employment, and household well-being.

Her concern was that policy had drifted toward minimizing the incidence of financial distress, often without enough regard for cost. That may have been understandable after 2008, she said, but over time it produced a one-directional precautionary ratchet. The result can be what she called “the financial stability of the graveyard”: apparent calm sustained by constraint rather than strength. Such a system, in her account, is poorly suited to an economy dependent on entrepreneurship, capital formation, and adaptation.

Skinner described Secretary Bessent’s reorientation around two propositions. The first is that growth is a foundation of financial stability. Growth improves balance sheets, raises incomes relative to liabilities, and improves the capacity of firms and households to service debt and absorb shocks. Weak growth or contraction, by contrast, exposes and amplifies vulnerabilities. Financial crises become economically damaging when disruptions to credit and confidence impair production, investment, and employment.

That means financial regulation cannot be evaluated only by its effect on measured risk inside the financial sector. It must also be judged by its effect on credit availability, market liquidity, productive investment, and the broader economy. A policy that looks stabilizing in the short term may, at sufficient scale, erode the conditions that make stability possible.

Her second proposition is that financial stability is inseparable from economic security. Systemic risk increasingly lies at the intersection of economics and geopolitics, she said. Financial systems are shaped not only by markets, but by strategic competition among states. A financial system rests on the productive capacity of the economy it serves, and that capacity depends on secure supply chains, reliable access to energy and critical inputs, and leadership in productivity-enhancing technologies.

When those conditions are strong, the financial system benefits from stable cash flows, predictable investment horizons, and resilient balance sheets. When they weaken, the effects can move quickly into markets through price volatility, liquidity stress, and uncertainty about returns. Many disturbances, Skinner argued, are not endogenous to finance; they are downstream expressions of structural vulnerabilities in the real economy, often intensified by geopolitics.

The operational implication is prioritization. Not all risks are equal, Skinner said, and attempting to enumerate every conceivable vulnerability can dilute focus and encourage an expansive but ineffective posture. FSOC also needs to consider cumulative policy effects, because rules may be adopted incrementally but experienced in the aggregate. And it needs an outward-looking strategic perspective, because the dollar, Treasury market functioning, and U.S. capital-market depth are pillars of the international economic order, not merely domestic concerns.

Skinner identified current FSOC priorities as Treasury market resilience, cyber risk and crisis preparedness, bank regulatory and supervisory modernization, artificial intelligence, and household financial resilience. In Q&A, she clarified what FSOC can and cannot do. It can set a public view of what counts as financial stability risk, shape the tone for markets, create data sets, build measurable indicators, and run scenario planning or tabletop exercises. It does not itself write the detailed prudential rules that determine the balance between risk-taking and safety; that belongs to prudential and market regulators.

That distinction shaped her answer to Ross Levine, who asked how a growth-oriented policy avoids encouraging excessive risk-taking and bailout expectations. Skinner said “failure to innovate, failure to compete, failure to take risk” can itself be a financial stability risk. She also said FSOC annual reports had become something like a “Hotel California” of risks: once a risk entered, it never left. The new approach, she said, is to prioritize a smaller set of actionable risks while still fulfilling statutory monitoring duties.

Her “Laffer curve for macroprudential policy” was the compact version of the argument. If regulation is always added after a crisis but never right-sized, modernized, or tailored to current conditions, she argued, the accumulation inevitably deters growth. That was not a claim that risk should be ignored. It was a claim that financial stability policy must govern risk without treating every reduction in visible risk as a net gain.

Decentralized finance exposes the same tradeoff between innovation and bailout risk

Ross Levine pushed the presenters toward the unresolved problem. Populist anger at centralized, elite, opaque institutions can create support for deregulation or decentralized finance. But if investors still expect the Fed to bail out the system in a crisis, deregulation can also encourage excessive risk-taking. The question was how those incentives evolve.

Marvin Barth answered as a political economist, not as a designer of a prudential regime. He said he disagreed strongly with Barry Eichengreen and Ken Rogoff on stablecoins and narrow banking. In his view, stablecoins and narrow banking are taking off because a populist base wants decentralization, distrusts banks, and distrusts bureaucratic regulators. Earlier anti-bank movements lacked a working technology; this one has one.

Barth said global remittances in dollars on stablecoins are approaching foreign direct investment into the United States in magnitude and growing at about 50 percent a year. He also emphasized that crypto interests now have political-economy resources. His anecdote was a client who made his money in crypto and came to lunch in a custom Savile Row silk sweatsuit costing $5,000. The point was not the suit; it was that the coalition has money. “They have money, and they’re using it to get this stuff done,” Barth said. His forecast was a path toward narrow banking alongside deregulation of the banking system.

Darrell Duffie answered Levine’s balance-sheet question with caution. The Fed should not pursue any of his options without careful cost-benefit study, he said. Liquidity-regulation changes and payment-system redesign are partly substitutes: if banks are comfortable using Fed liquidity facilities or overdrafting, they need not hoard as many reserves; if payment systems are more efficient, the same is true. If forced to choose, Duffie said he would pick one of those two paths before trying both. Temporary open market operations are easier but limited. Tiering reserve remuneration would likely be powerful, but extremely difficult to sell to the banking lobby because of its effect on bank profitability.

Audience questions sharpened the innovation problem. Yuriy Gorodnichenko asked how much extra growth and how much added risk would result from undoing Dodd-Frank, and whether FSOC had studied the tradeoff. Bill Nelson asked Skinner whether stablecoin issuers backing coins with uninsured bank deposits could create a financial stability risk if runs forced those deposits out of the banking system. Michael Bordo posed the broader question: how can policymakers know whether financial innovation — stablecoins, private equity, or other developments — will create systemic risk, without either stifling innovation or assuming it will all work out until a crisis arrives?

Nelson also challenged Duffie on whether tiered reserves are, in effect, a return to scarce-reserves logic. In Nelson’s framing, paying below-market rates on excess reserves is what gives banks an incentive to economize on reserves, turn first to each other for liquidity, and revive interbank markets. Mickey Levy asked whether the Fed’s concept of “ample” reserves reflects excessive aversion to short-term funding-market volatility and a tendency toward fine-tuning.

Duffie’s answer was that tiering need not recreate the pre-crisis scarce-reserve regime. In the earlier system, if the Fed missed, the spread could be hundreds of basis points and banks would be desperately scrounging for reserves at day’s end. A tiered system with still-large reserve balances would be different. The market rate would settle between the upper and lower tiers; if the Fed missed by some amount, Duffie said, it would not be catastrophic, rates would not spike by 300 basis points, and payments would not be missed in desperation. The shadow cost of an additional dollar of reserves would be far lower in a still-ample system than in the old scarce-reserve regime.

Barth took the final word on Bordo’s innovation question by returning to Bordo’s own long-ago advice to him: use theory, history, and more than models. Innovation is precisely where policymakers will not already have a model, Barth said. The problem requires all available faculties of analysis. Even after centuries of central-bank history, he noted, the conference was still debating how to shape central banks appropriately. “It takes time,” he said.