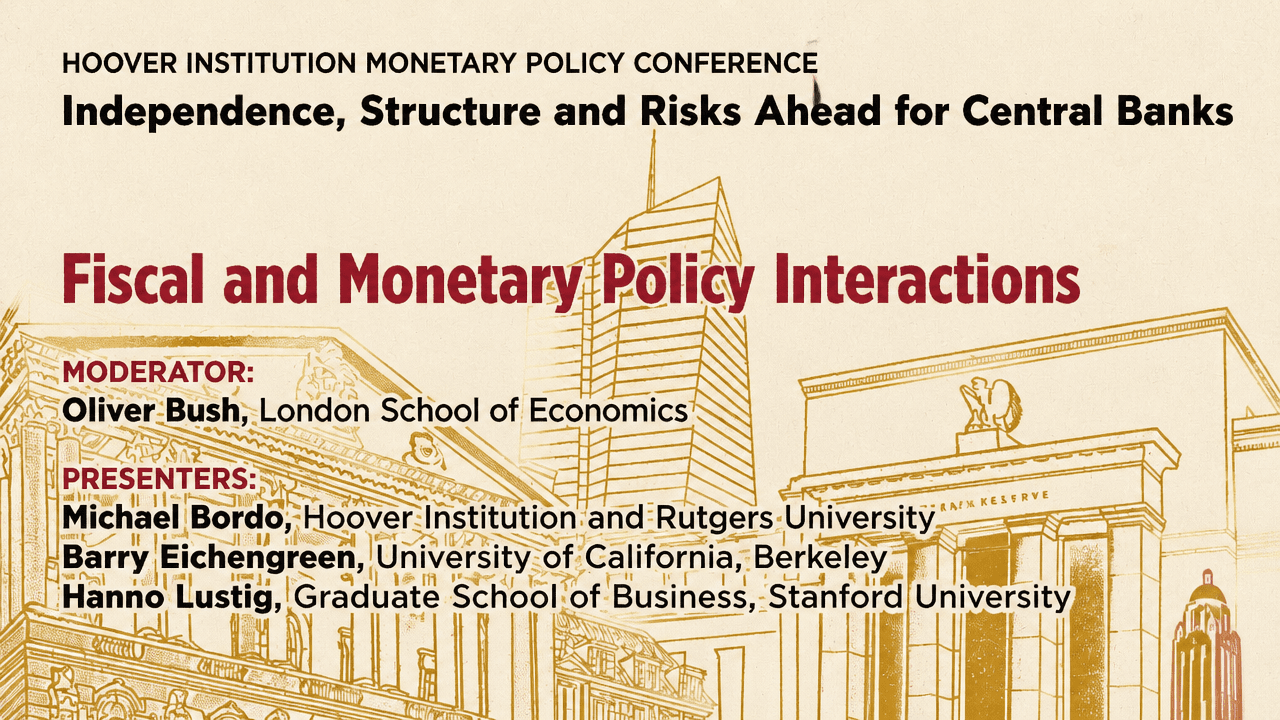

Fiscal Stress Is Narrowing the Room for Independent Central Banks

Michael Bordo

Michael Bordo Barry Eichengreen

Barry Eichengreen Samim Ghamami

Samim Ghamami Marvin Barth

Marvin Barth Oliver Bush

Oliver Bush Alejandra Edwards

Alejandra Edwards Hanno Lustig

Hanno Lustig Thomas HoenigHoover InstitutionMonday, June 1, 202621 min read

Thomas HoenigHoover InstitutionMonday, June 1, 202621 min readAt a Hoover Institution conference on central-bank independence, Michael Bordo, Barry Eichengreen and Hanno Lustig argued that fiscal policy is increasingly constraining what monetary policy can credibly do. Bordo used Britain’s Great Inflation to show how a fiscal regime shift can turn shocks into inflation; Eichengreen said U.S. fiscal politics now pose risks to the dollar and the Federal Reserve; and Lustig argued that markets are starting to price Treasurys less as safe assets than as risky debt. Their shared point was that legal independence offers central banks only limited protection when debt dynamics, fiscal politics and bond-market stress move against them.

Fiscal stress changes what monetary policy can do

Fiscal and monetary policy were treated here not as separate domains that occasionally collide, but as a single system whose balance depends on how governments finance fiscal shocks. The shared concern was that high debt, weak fiscal adjustment, and bond-market fragility can reduce the practical space in which central banks operate — even where legal independence remains intact.

Oliver Bush framed the issue with Mervyn King’s 1995 remark that central banks, despite being accused of obsessing over inflation, were if anything obsessed with fiscal policy. Bush noted that public central-bank speeches do not show a simple upward trend in references to fiscal policy alongside rising debt-to-GDP ratios. They do show spikes around the global financial crisis and in 2020, though the 2020 pickup was shorter-lived. Public speech, he suggested, is an imperfect guide because fiscal policy is difficult for central bankers to discuss openly.

His historical example came from the United Kingdom in 1976, when Bank of England and Treasury officials considered instruments for hitting monetary targets. They concluded that interest rates, “in the present conjuncture of a continuing high PSBR,” would not be particularly effective in restraining monetary growth, because higher debt sales would be largely offset by higher debt-interest payments. Bush read this as an early grasp of the logic later associated with unpleasant monetarist arithmetic: if fiscal financing is not disciplined, monetary tightening can be undermined by the fiscal consequences of the tightening itself.

That concern ran through the three presentations. Michael Bordo argued that the United Kingdom’s Great Inflation had a distinct fiscal footprint. Barry Eichengreen argued that U.S. fiscal weakness now matters for the dollar’s global role and for pressure on the Federal Reserve. Hanno Lustig argued that markets seem to have begun treating U.S. Treasurys less like safe debt and more like risky debt, while policymakers still largely operate with models in which government debt is safe.

The disagreement was not about whether central banks should care about fiscal policy. All three treated that as unavoidable. The harder questions were how fiscal dominance should be recognized, what central banks can credibly commit to, and when bond-market intervention preserves market functioning rather than suppressing price discovery.

Bordo’s UK case: the Great Inflation followed a fiscal regime switch

Michael Bordo presented the United Kingdom’s Great Inflation as a case in which fiscal institutions and expectations changed first, with inflation following from the new regime interacting with bad policy and bad luck. He contrasted this with the standard U.S. account, where the Great Inflation is often told as a story of Federal Reserve mistakes under William McChesney Martin and Arthur Burns, corrected under Paul Volcker. For the United Kingdom, Bordo argued, the decisive change was fiscal: a move away from a long-standing commitment to stabilize public finances and later a return to that orthodoxy.

The historical baseline was what Bordo called the Treasury View. For most of British history, he said, governments borrowed in wartime but were expected to run primary surpluses in peacetime to stabilize or repay debt. The view was associated with institutions such as sinking funds and terminable annuities, and with political figures including Robert Walpole and William Gladstone. Bordo linked this to Robert Barro’s later term “tax smoothing”: wars could be financed by borrowing, but the peacetime fiscal path had to validate the debt.

The narrative evidence came from Budget speeches. Bordo, Bush, and Ryland Thomas use those speeches, running back to the eighteenth century, to identify what fiscal objectives policymakers said they were pursuing. They supplement that with empirical work showing how fiscal shocks were financed in different regimes. According to Bordo, expansionary fiscal shocks were financed by higher primary surpluses in the classical gold standard era up to 1914, but by higher inflation in the 1960s and 1970s.

The postwar break came after the Bank of England was nationalized in 1946 and the Treasury took control of macroeconomic policy. Keynesian demand management displaced debt stabilization as the central fiscal objective. Bordo quoted postwar Chancellor Hugh Dalton’s 1954 statement that Britain could free itself from “the old and narrow conception of balancing the budget” and move toward “the new and wider conception of the budget balancing the whole economy.” By the mid-1950s, Bordo argued, the traditional debt-stabilization objective had been abandoned.

That abandonment mattered most once external constraints weakened. Under Bretton Woods, Britain’s fixed exchange-rate commitments still acted as a constraint: too much expansion could produce a balance-of-payments crisis. After the Nixon shock and sterling’s float, Bordo argued, the United Kingdom had no nominal anchor between 1972 and 1976. The fiscal regime was active, the monetary regime passive, and fiscal shocks could be financed in part by unexpected inflation.

Bordo connected this explicitly to modern fiscal theories of inflation. A fiscal financing regime, in his definition, is a set of arrangements, institutions, and expectations determining how fiscal shocks are financed. Drawing on John Cochrane’s framework, he said fiscal shocks can be absorbed through future surpluses, growth, inflation, or financial repression through artificially low real interest rates. If fiscal policy is not used to stabilize debt, inflation may become the mechanism that resolves fiscal imbalance. Under such a regime, he said, tighter monetary policy may even worsen inflation — the “stepping on a rake” logic he associated with Christopher Sims.

When fiscal policy isn’t used to stabilize debt, inflation can be the mechanism by which the imbalances are resolved.

Bordo’s account of the inflation episodes was structured around the interaction of regime, policy, and shocks. In the 1960s, British policymakers used expansionary fiscal policy in “go-stop” fashion, partly under the influence of growth theories associated with Roy Harrod and Nicholas Kaldor. Fiscal expansion was intended to raise growth, but Britain’s open-economy constraint repeatedly produced currency pressure, outside rescues, and reversals. Devaluation followed in 1967.

The larger break came in 1972–75. With the nominal anchor gone, Chancellor Anthony Barber’s “go-for-growth” Budget produced rapid nominal and real expansion. Bordo said real GDP growth peaked at 10% and nominal GDP growth at 20% in early 1973; broad money growth reached up to 30%, credit growth up to 40%, and both were fueled by banking deregulation. Significant fiscal and current-account deficits appeared by 1973. Two weeks before the first oil shock, Britain agreed an incomes policy that built automatic wage responses to price increases into the system. Earnings growth peaked above 30% in 1975, and inflation reached 25%.

The 1976 crisis was the turning point. A currency crash led to an IMF rescue package based on monetary targets and fiscal conditions. Bordo emphasized Prime Minister James Callaghan’s rejection of the Keynesian consensus: “We used to think that you could spend your way out of a recession and increase employment by cutting taxes and boosting government spending. I tell you in all candour that that option no longer exists.” Bordo described that as the moment when Britain began moving back toward the Treasury View, though he also noted backsliding in 1977 and 1978 through expansionary fiscal policy and overshooting of monetary targets.

The final inflation episode involved the second OPEC shock, labor unrest, the Winter of Discontent, and the Thatcher government’s Medium-Term Financial Strategy. The new approach combined monetary targeting with an effort to rebalance away from public-sector borrowing and toward private investment. Bordo highlighted the 1981 Budget, which tightened fiscal policy despite a downturn, as evidence of renewed fiscal discipline. By the early 1990s, he argued, fiscal credibility had been rebuilt: unlike in the mid-1970s, early-1990s deficits were not associated with high inflation, which he said suggested confidence that they would be paid for with future surpluses.

His conclusion was that postwar Britain provides a case study of fiscal inflation. In his account, it was made possible by a fiscal financing regime switch, amplified by bad policy and adverse shocks, and ended only when fiscal orthodoxy was rediscovered and monetary policy again had a nominal anchor to work with. Bordo said the history “resonates” with what happened in 2021 and referred to John Cochrane’s comparison with World War II: a huge fiscal shock, accommodated by the Fed. He presented that as something to learn from, not as a complete causal account of post-pandemic inflation.

Eichengreen’s dollar risk starts with fiscal politics

For Barry Eichengreen, the dollar risk begins before any visible break in inflation or exchange rates. If investors come to doubt U.S. debt sustainability, they may also expect the Federal Reserve to face pressure to keep rates low in order to ease the debt-service burden. In his chain of concern, low rates could fuel inflation and dollar depreciation; losses on U.S. Treasury securities could encourage foreign private and official investors to diversify away from dollar assets; and if doubts about Fed independence rise, some diversification could occur before inflation and depreciation themselves materialize.

He described this as one factor weighing on the dollar’s global role, not a completed causal sequence. The reserve-currency evidence he presented pointed to gradual erosion rather than a sudden break. In the chart he discussed, the dollar’s share of allocated global foreign-exchange reserves had declined from a bit above 70% around the turn of the century to a bit below 60% today. Eichengreen said exchange-rate adjustments smooth the line but do not change the start and end points. A separate LSEG Datastream chart put foreign central-bank holdings of U.S. Treasurys at 14% of total Treasury securities outstanding, down from a record high of 40% in June 2008.

Eichengreen did not present fiscal concerns as the only threat to dollar dominance. He also listed financial-stability worries from private credit, crypto, and bank supervision; doubts about whether Fed swap lines would continue if the Fed became less independent or more narrowly focused on its domestic mandate; tariffs and trade policy; increasing U.S. recourse to sanctions; weakening alliances; and general U.S. economic-policy uncertainty. He said European counterparts ask whether they should continue relying as heavily on the United States for national defense, and by extension whether they should rely as heavily on the dollar and U.S. correspondent banking system.

The fiscal part of the argument rested on two empirical claims. First, in work with Serkan Arslanalp on living with high public debt, he found only two robust correlates of successful sustained debt stabilizations: high growth and low political polarization. Growth stabilizes the denominator of the debt-to-GDP ratio. Low polarization allows political factions to compromise on chronic deficits and maintain a fiscal strategy across changes of government.

The United States, in his telling, does poorly on the second condition. Drawing on survey-based measures of affective polarization, Eichengreen said the U.S. has the highest level among advanced economies, and that the level has been rising. He declined to choose among theories for why polarization has risen, but treated the pattern as an obstacle to fiscal consolidation.

Growth could help, especially if artificial intelligence raises productivity. Eichengreen was cautious. He said estimates of AI’s productivity effect are “all over the map,” as are estimates of when any macro-level effect will become visible. A Goldman Sachs Research item he cited estimated U.S. potential GDP growth at 2.3% in 2025 and forecast 2.3% over 2026–2028, with economywide productivity growth holding steady at 2% per year but labor’s contribution slowing because of lower immigration and population aging. Eichengreen used the report as an example of why he does not assume AI will solve the debt arithmetic.

His second empirical claim concerned the fiscal response function. He argued that the familiar Bohn test — whether the primary surplus rises in response to higher debt — may miss the historically relevant variable. In work with Maxime Menuet, Eichengreen finds that the primary surplus historically responds not to the stock of debt, but to the flow of debt service as a share of GDP. Debt service is what appears immediately in the budget, while the debt stock does not.

In U.S. data from 1800 to 2023, he said, there is no robust response of the primary surplus to the debt ratio. The response appears instead when debt service rises in two settings: after major wars, and when the real interest rate minus the real growth rate is unfavorable, creating the risk of a debt snowball. That pattern matched Bordo’s Treasury View: deficits widen during wars and are followed by primary surpluses afterward.

The problem, Eichengreen said, is that this response has weakened. Regressions over the full 1800–2023 period are driven by pre-World War I data. After World War I, and especially after later conflicts, the stabilizing reaction is much less visible. There was little surplus response after Vietnam or the Iraq and Afghanistan wars. Warnings that U.S. debt service now exceeds defense spending have not elicited much response either. His conclusion was not that a dollar crisis is imminent, but that his pessimism about U.S. fiscal prospects remains intact, and that this makes him worry about the consequences for monetary policy.

Lustig’s Treasury-market warning is about competing models of debt

Hanno Lustig argued that the market’s model of U.S. Treasurys appears to have changed since 2020, while policymakers’ models have not. Before the pandemic, market participants treated Treasurys as safe assets in several reinforcing senses. Treasurys were expensive relative to close substitutes such as AAA corporate bonds and foreign sovereign bonds. They earned large convenience yields, reflecting safety and liquidity. The stock-bond correlation was negative, making Treasurys a hedge against equity risk. In stress events, investors exhibited flight to safety and Treasury yields fell.

The evidence he emphasized was comparative pricing. Against AAA corporate bonds adjusted for credit risk, Lustig said the pre-pandemic positive spread has largely vanished, especially at longer maturities. Investors are now close to indifferent, in his interpretation, between AAA corporates and Treasurys after adjusting for credit risk. Against G10 foreign sovereign bonds hedged into dollars, he said the picture is similar. At longer maturities, he argued, the gap has flipped sign, suggesting that investors may now prefer a German bund to a U.S. Treasury. His summary was that U.S. Treasurys are no longer expensive relative to close substitutes.

The stock-bond correlation has also flipped sign. Lustig used stress-event examples from the April 2025 “Liberation Day” tariff announcement and the March 2026 Iran war. In both cases, the stock market fell, but Treasury yields rose. That is the opposite of the usual flight-to-safety pattern he described as pre-2020 behavior.

He also pointed to evidence that debt valuation now responds directly to fiscal news. His preferred example was the House consideration of the “One Big Beautiful Bill” in May 2025. Using minute-by-minute data, he compared returns on the full Treasury portfolio, S&P 500 returns, and the probability of House passage inferred from prediction markets. As the probability of passage of what he described as fiscally bad news rose, both bond and stock returns corrected. For Lustig, this was evidence that the valuation of government debt is starting to respond to fiscal shocks.

The conceptual shift, as he framed it, is from safe debt to risky debt. In a safe-debt regime, the central bank is the leading authority, large government-spending shocks are expected to be fully funded by future taxes, and Treasury yields do not respond much to fiscal news. In a risky-debt regime, the government is in the driver’s seat, bondholders bear the risk of unfunded spending shocks, and Treasury yields, term premia, and long-run expected inflation can respond to fiscal news. Debt is continuously marked to market.

| Question | Safe-debt model | Risky-debt model |

|---|---|---|

| Leading authority | Central bank | Government |

| Who bears unfunded spending risk | Taxpayers through future funding | Bondholders through mark-to-market losses |

| Treasury-yield response to fiscal news | No | Yes |

| Response to market stress | Flight to safety | Mark-to-market repricing |

| Stock-bond correlation | Negative | Positive |

| Policy interpretation of rising yields | Market dysfunction or plumbing | Market functioning or fiscal news |

Lustig’s concern is that central banks and financial regulators still tend to use safe-debt models. Macro models often assume government spending is fully funded and leave little role for the government-debt valuation equation. Regulatory models also treat government debt as safe through risk weights and money-market-fund rules. This creates a tension: when yields rise in response to fiscal news, policymakers using a safe-debt model may interpret the move as market dysfunction, a microstructure problem, or a plumbing issue. Market participants, using a risky-debt model, may view the same move as appropriate price discovery.

The risk, Lustig said, is that central banks use large balance sheets to “fix” plumbing problems that are not really plumbing problems. He described this as a risk and a possible result of competing models, not as proof that every intervention has this character. His concern is that relabeling fiscal news as plumbing can blunt market discipline and delay fiscal correction.

The United Kingdom’s 2022 mini-budget supplied his clearest illustration. Chancellor Kwasi Kwarteng announced £45 billion of unfunded tax cuts, and gilt yields rose sharply during the announcement. Lustig said the initial bond-market response was hard to dispute as fiscal news: the Chancellor was announcing large unfunded tax cuts. But the situation became a financial-stability problem because pension funds had highly leveraged gilt exposures and faced margin calls, leading the Bank of England to pause quantitative tightening only a week after starting it. Fiscal news and market plumbing were intertwined.

He sees a similar fragility in the U.S. Treasury market. The Treasury is relying increasingly on bill issuance, where some convenience yield may remain, while longer-maturity convenience yields have eroded. With the Fed stepping back and primary dealers having limited balance-sheet capacity, Treasury issuance is increasingly absorbed by hedge funds through the basis trade. Lustig called that a fragile arrangement. Fiscal challenges and Treasury-market plumbing, he said, are not mutually exclusive; they can reinforce one another.

But he also argued that fiscal policymakers need market discipline. CBO long-term projections in his slides put deficits, net interest, and federal debt on an adverse path over the next 30 years. Lustig described those numbers as projections rather than forecasts, and said that in the United States market discipline is probably the only way deficits are brought down. If every adverse bond-market response to fiscal news is relabeled as plumbing, he argued, that discipline is weakened.

His warning extended to balance sheets and financial repression. A BlackRock chart, which Lustig said he first saw presented by Olivier Jeanne, plotted the share of government debt held by banks and central banks against government debt-to-GDP ratios. His reading was that as debt-to-GDP keeps rising, banks and central banks end up being forced, one way or another, to absorb issuance. That raises risks of inflation, financial repression taxes, and related distortions.

Independence is protection, not a fiscal solution

Asked by Oliver Bush whether fiscal stress strengthens or weakens the case for central-bank independence, the panelists agreed that independence is not a complete shield. They differed in emphasis.

Hanno Lustig said central-bank independence will probably not protect central banks completely from fiscal problems. In his view, large issuance and an adverse fiscal trajectory make bond-market stress events easy to imagine. If market participants push yields up in response to fiscal shocks and that triggers stress, a central bank may find it very hard to commit not to intervene. He had already given the United Kingdom as an example; he also said examples could be drawn from the eurozone. For Lustig, the only real solution is a more sustainable fiscal trajectory. It would be a mistake, he said, to sell central-bank independence as the fix.

Barry Eichengreen agreed that “actual existing central bank independence” does not protect central banks completely from fiscal-policy pressures, or from many other pressures. But he called it the best protection they have. Monetary policy cannot solve fiscal problems, but central bankers cannot ignore them. Eichengreen’s prescription was mandate discipline: central bankers should speak forcefully and transparently about fiscal imbalances insofar as those imbalances affect the central bank’s ability to achieve its explicitly defined mandate — inflation, employment, financial stability, and the policy settings needed for those goals. The rest should be left to other branches and agencies.

Michael Bordo gave the starkest historical answer. If a fiscal shock is big enough, he said, the central bank loses its independence. In countries with small deficits and low debt ratios, this is not the issue. But if the fiscal shock is large and the debt ratio is going to rise materially, “that’s it for central bank independence.”

The exchange exposed two levels of the problem. Legal independence can help a central bank resist ordinary political pressure. But the panelists treated fiscal dominance as a constraint created by the state’s consolidated balance sheet, not just by political interference. If fiscal choices make debt dynamics unstable, the central bank may face pressure through bond markets, financial stability, and debt-service arithmetic even without a formal change in its statute.

The challenges sharpened the evidence, not the basic tension

The most material audience challenges tested whether the evidence for dollar diversification and Treasury repricing was being overread.

Marvin Barth argued that the dollar-reserve chart looks different if one backs out particular central-bank holdings by currency. He said the diversification story is mainly about Russia and China, driven by payments issues rather than currency issues, and pointed to Chinese willingness to accumulate dollar claims. He also argued that stablecoins, which he said are more than 99% dollar transactions, point in a different direction. On Lustig’s charts, Barth questioned whether the AAA-Treasury and foreign-sovereign comparisons reflected measurement issues, including the CDS treatment and the role of FX swaps and post-Basel III widening of the dollar basis.

Eichengreen disputed the claim that the dollar-reserve decline is only a Russia-China story. Looking at the twenty-first century as a whole, he said the trimming of the dollar share has been widespread across scores of countries. Of the roughly 15 percentage points lost by the dollar in global reserve share over those 25 years, he said one quarter was gained by the Chinese renminbi and three quarters by nontraditional reserve currencies: currencies of small, open, well-managed, generally inflation-targeting countries. He said more than 50 countries have moved away from the dollar at the margin toward alternatives that have become easier to trade and use through digital platforms. He dismissed stablecoins as a “complete non-issue” for the reserve-currency questions under discussion.

Lustig agreed that covered-interest-parity violations have grown since 2008, but said that was not what his chart was measuring. He was comparing Treasurys with sovereign bond yields hedged back into dollars using forward contracts and cross-currency basis swaps in the background. He said there is no mechanical relation between the increased size of the basis and the pattern he showed, and that the disappearance of the earlier gap between Treasury yields and foreign yields hedged into dollars is a novel development not reducible to constrained banks widening the basis. On the CDS adjustment, he said not subtracting CDS from Treasurys does not matter quantitatively.

Alejandra Edwards asked whether Social Security and Medicare were included in Lustig’s fiscal projections. Lustig said the CBO projections include them. His understanding was that the CBO rolls forward current law except that, for Social Security, it assumes the federal government keeps its promises when the trust fund runs out. That assumption, he said, is a large part of the projected deficit.

Samim Ghamami pressed on whether an inflation-targeting central bank following the Taylor principle can become dysfunctional when public debt and deficits are not sustainable, and on whether Treasury-market microstructure fixes should be dismissed as mere relabeling. Lustig’s answer preserved the distinction he had been making: he was not denying that real plumbing problems exist or that there can be a good case for addressing them. His objection was to always relabel fiscal-news events as plumbing issues, because that gives fiscal policymakers the impression that the only bond-market problems are technical. In many cases, he said, the fundamental issue is an unsustainable fiscal path, and central banks should be more transparent about that.

A new accord would draw a boundary around Treasury-market support

Thomas Hoenig raised the question of a new Fed-Treasury accord. His premise was that the United States is in or near fiscal dominance and that the Fed has implicitly accepted responsibility for stable and highly liquid Treasury markets. A new accord, as he framed it, would require the Fed to reject automatic responsibility for supporting Treasury-market liquidity beyond some point and force Congress and the Treasury to address fiscal problems. Without such a boundary, he said, it is hard to see how the problem is solved.

Lustig was sympathetic to the direction of Hoenig’s concern, while not setting out a complete accord design. He said he had recently been reading about the 1951 Fed-Treasury Accord and found it striking that many Fed officials at the time believed real price discovery in the Treasury market required convincing market participants that the Fed would never again intervene as it had during and after World War II. He contrasted that with the current belief that bond markets work well only if participants expect the Fed to intervene every other year. “Something seems off about that,” he said. In his view, real price discovery would require stronger confidence that central banks will not automatically intervene.

Eichengreen was more cautious. He described Hoenig’s idea as a new “anti-accord” or “discord” and warned that opening that door could produce an outcome its advocates might not like. His concern was institutional: renegotiating the Fed-Treasury relationship under fiscal stress could invite pressures or constraints worse than the current ambiguity.

Bordo saw continuity with older monetary debates. He recalled Milton Friedman’s criticism, in A Program for Monetary Stability, that the Fed did debt management. The same conflict remains: a central bank charged with monetary policy becomes entangled in concerns about government debt. Bordo said there is room at least to lay out what an accord would be.

A final challenge went to the word “unsustainable.” An audience member argued that warnings about peacetime deficits leading to higher inflation or higher interest rates had circulated since the 1970s without materializing in the expected way. He accepted that the budget process is dysfunctional and that entitlement compounding affects resource allocation, but asked economists to do better than simply label the current budget path unsustainable.

Lustig replied that American exceptionalism may make U.S. observers too optimistic because the United States has not experienced a fiscal crisis. He said arguments from the 2010s for not worrying about deficits no longer apply: it is no longer obvious that the real interest rate is below the growth rate. The United States benefited for a time from strong foreign demand for Treasurys and from the Fed as a large, price-insensitive buyer. Both have stepped back, and yields have responded. Still, he added, market participants may price in possible future interventions when valuing ten-year yields.

Eichengreen accepted that “unsustainability” can be a weasel word or convenient shorthand. He did not recommend solving that by building ever more refined debt-sustainability models. Instead, he argued for specifying the different channels through which a rapidly growing debt ratio affects variables policymakers care about. Bordo ended on the practical difficulty: if the debt is rising because entitlements keep growing, it is hard to say how the United States gets out of the problem.