Uber Says US Demand and Cost Discipline Can Offset Macro Pressure

Uber CFO Balaji Krishnamurthy told Bloomberg Tech that the company’s latest forecast reflects sustained demand from riders and travelers despite a more uncertain macro and geopolitical backdrop. He argued that Uber is pairing product expansion, including hotel bookings through Expedia and a larger Uber One base, with tighter operating discipline and AI-driven efficiency. Krishnamurthy framed the quarter as evidence that Uber can keep growing by widening its consumer and enterprise use cases while controlling costs.

Uber is presenting growth and cost discipline as the answer to a choppier backdrop

Balaji Krishnamurthy pointed to 21% topline growth, 44% year-over-year EPS growth, and a 10x year-over-year increase in Uber’s nascent autonomous-vehicles business as evidence that demand is holding up while the company manages costs. Asked by Caroline Hyde how Uber is still pushing bookings and demand amid macro concerns and oil-price pressure, Krishnamurthy said Uber is pairing product expansion with “extremely disciplined operations” and increasing use of AI to drive efficiency.

He tied the demand case to Uber’s recent product expansion. At the company’s annual Go-Get event, he said, Uber introduced new products and features designed to “meet our customers where they want to go,” some built internally and others developed through partners such as Expedia. That expansion, he said, is meant to bring “best-of-breed solutions” into Uber’s own consumer surface area.

The company’s 21% quarterly growth, Krishnamurthy said, marked the third consecutive quarter at roughly that level. He added that Uber’s outlook “met and exceeded expectations on both top and bottom line,” framing the quarter as a combination of demand momentum and operating leverage rather than demand alone.

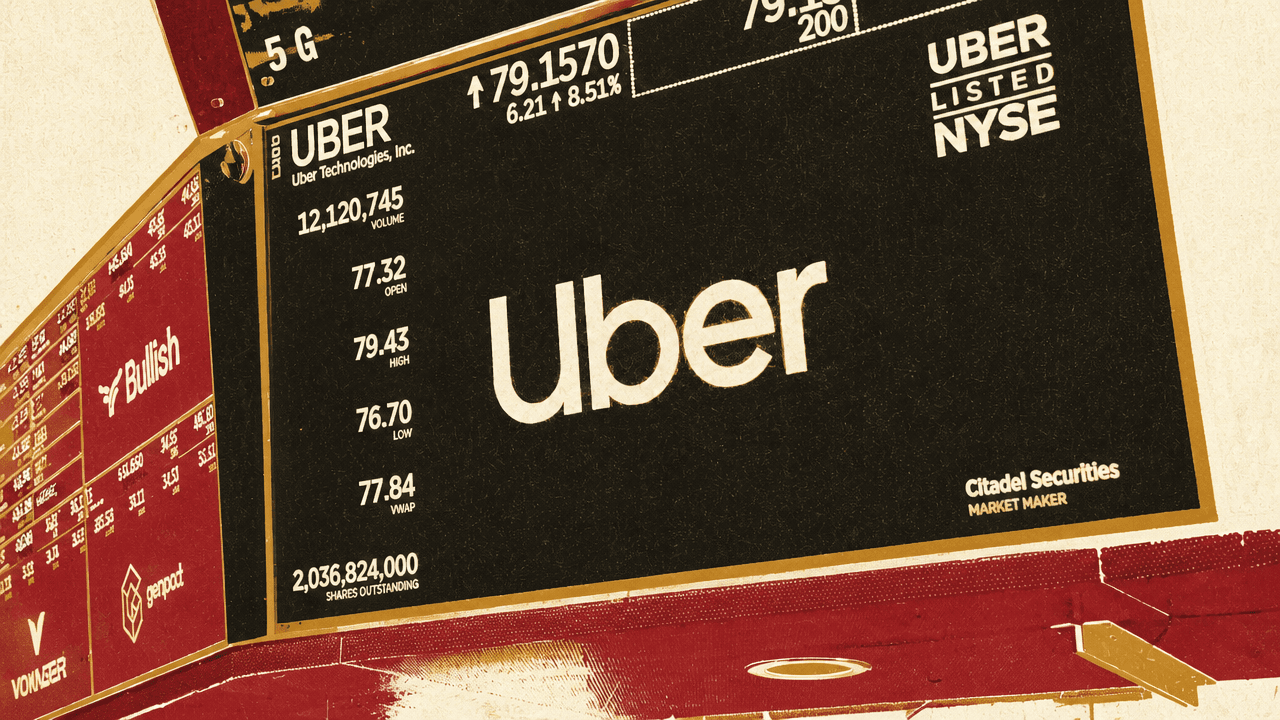

Bloomberg Tech’s on-screen market graphics showed the stock reaction across three time frames: Uber at $79.03, down 7.92% on the one-year view; $79.03, down 3.28% year to date; and about $79.08, up 8.40% intraday. The displayed equity picture was therefore mixed: positive on the day, negative on the longer views shown during the segment.

Expedia adds a travel-adjacent use case to Uber’s cross-platform loop

The Expedia partnership adds hotel bookings to Uber’s app, but Krishnamurthy placed the move inside a broader objective: increasing the share of consumers who use more than one part of Uber’s platform. Today, he said, only about 20% of Uber’s monthly active consumers engage across both mobility and delivery. Those customers are materially more valuable to Uber because they generate significantly higher gross bookings profits.

| Metric | Figure Krishnamurthy gave |

|---|---|

| Monthly active consumers using both mobility and delivery | About 20% |

| Uber One members | About 50 million |

| Uber One members added in the last year | About 20 million |

| Gross bookings driven by Uber One members | 50% |

The company’s subscription product, Uber One, sits underneath that behavior. Krishnamurthy said Uber One reached about 50 million members this quarter, after adding about 20 million members over the past year. Those members now account for 50% of Uber’s gross bookings.

When you think about a partnership like Expedia, what we are trying to do is to expand the surface area of what we consider cross-platform.

Krishnamurthy described hotels as adjacent to Uber’s existing travel behavior: 15% of Uber’s mobility gross bookings come from airport trips, 40% of US riders take trips outside their home cities, and Uber handled 1.5 billion trips globally last year that happened outside users’ home cities.

Expedia supplies hotel inventory and pricing; Uber adds the booking surface and a platform incentive. Krishnamurthy said the partnership allows Uber to bring Expedia’s hotel prices to consumers while giving them 10% cash back, which they can then spend on Uber. Hotels add another travel-adjacent use case that can feed Uber One and broaden cross-platform engagement beyond the core mobility-and-delivery pairing.

The B2B target depends on scaling Uber’s services through organizations

Uber’s business-to-business operation is already a $5 billion gross bookings business, according to Balaji Krishnamurthy, and the company wants it to become a $10 billion-plus business. He said the segment is growing 45%, well above the companywide 21% growth figure he cited earlier.

He described the B2B business as Uber’s mobility and delivery services offered in an “enterprise grade” format to customers across the corporate stack. That means the same underlying Uber services, but packaged for organizations rather than only individual consumers.

The scale argument rests on account penetration. Krishnamurthy said about 300,000 organizations globally currently use Uber through this offering. Over time, he said, Uber believes it can serve as many as 1 million organizations globally. That expansion, in his view, is what would allow the business to move from $5 billion to $10 billion in gross bookings.

| B2B measure | Current or target figure |

|---|---|

| Current gross bookings | $5 billion |

| Growth rate | 45% |

| Current organizations using the offering | About 300,000 globally |

| Potential organizations Uber says it can serve | As many as 1 million globally |

| Gross bookings ambition | $10 billion-plus |

The consumer and enterprise arguments are structurally similar. On the consumer side, Uber is trying to make rides, delivery, subscriptions, travel, and hotel bookings reinforce one another. In the enterprise business, it is trying to take mobility and delivery into organizational workflows at larger scale.