Snowflake Raises Outlook After $6 Billion Amazon Cloud Agreement

Snowflake CEO Sridhar Ramaswamy told Bloomberg that the company’s stronger outlook reflects AI-driven demand for its data platform, not a threat to its software model. He argued that Snowflake’s $6 billion multiyear Amazon agreement will lower infrastructure costs, support cheaper AI pricing for customers and strengthen joint selling, while product adoption and revenue metrics show AI increasing consumption on the platform.

Snowflake’s quarter pairs a stronger outlook with a $6 billion Amazon scale bet

Sridhar Ramaswamy framed Snowflake’s results as evidence that AI is increasing the value of the company’s data platform, while the company’s $6 billion multiyear agreement with Amazon is meant to make that usage cheaper and easier to sell at scale.

The operating metrics were the basis for Snowflake’s stronger annual outlook. Ramaswamy called it a “landmark quarter,” citing the strongest sequential dollar growth in the company’s history, product revenue of $1.334 billion, product revenue growth of 34%, and net revenue retention of 126%. Snowflake raised its annual product revenue growth guidance from 27% to 31%.

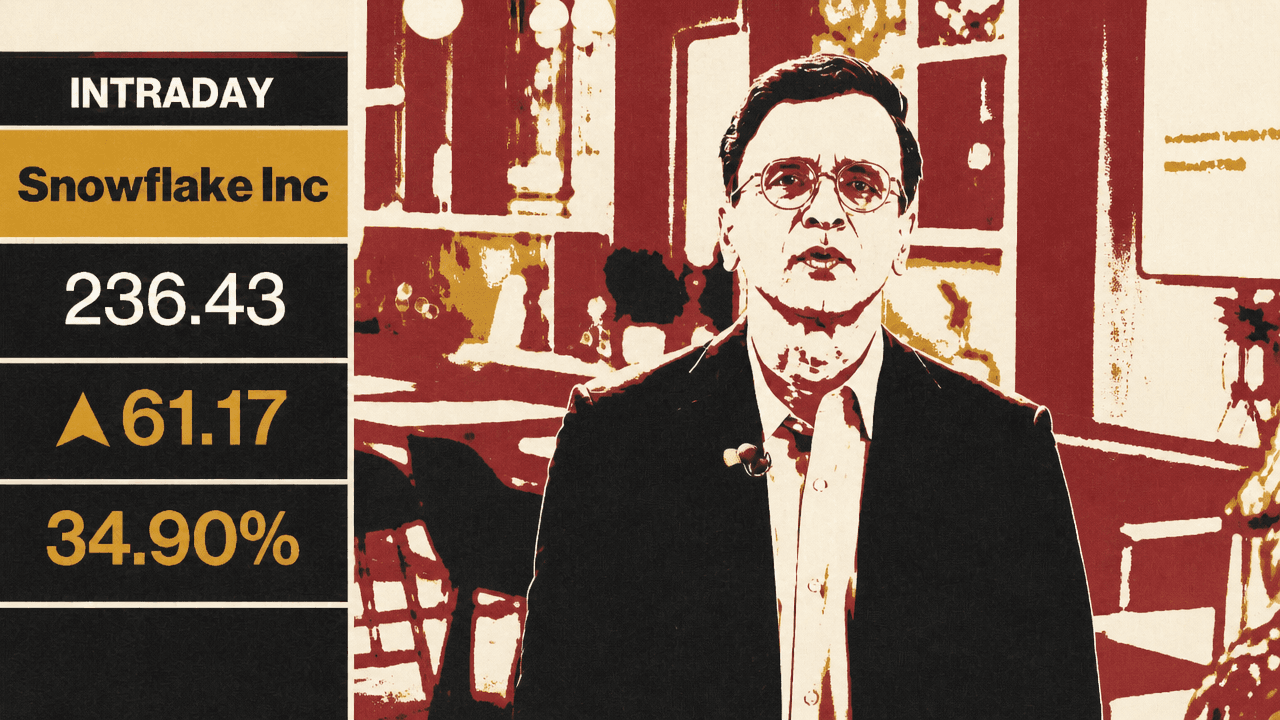

A Bloomberg chart shown during the discussion displayed Snowflake’s year-to-date stock performance declining from January into May before a sharp spike at the end. The on-screen quote showed Snowflake at 236.99, up 17.63, or 8.04%, at that moment. Separately, Caroline Hyde opened by saying Snowflake had added $20 billion to its market capitalization.

Ramaswamy’s larger claim was that the quarter showed “AI is compounding Snowflake’s advantage in data.” Matt Miller put the investor concern directly: for a long period, the market narrative had been that AI might disrupt software; in Snowflake’s case, he suggested, the quarter and the Amazon agreement raised the possibility that AI may instead accelerate software revenue.

Ramaswamy’s answer rested on Snowflake’s consumption model. A data platform that charges based on the value customers receive is helped, in his view, when AI allows customers to get more value from data already sitting in Snowflake. Historically, he said, customers built dashboards on top of the platform. With Snowflake Intelligence, the company is trying to put “all of the power of the data” and the applications users need inside a work agent. He also referred to “meaningful token consumption” on top of the platform as part of the AI opportunity.

He tied that argument to product adoption rather than AI positioning alone. Snowflake Intelligence, which he described as the company’s work agent, doubled adoption by accounts. Snowflake’s coding agent, which he referred to as “Co-co,” is used by more than 7,000 accounts. Those adoption figures, he said, are part of what gives Snowflake confidence in the business.

The Amazon deal is about lower AI pricing, bulk purchasing and joint selling

The $6 billion Amazon agreement is not presented by Snowflake as a chip-efficiency story alone. Ramaswamy said Amazon is Snowflake’s largest cloud service provider, while Snowflake also runs on Azure and Google Cloud. The importance of the Amazon agreement, in his telling, is scale: Snowflake can buy infrastructure capacity with confidence, get “massive economies of scale,” and pass some of those savings back to customers.

That point connects directly to Snowflake’s AI pricing. Ramaswamy said Snowflake announced a “huge change” in how it prices AI, making AI “a lot less expensive” for customers. Deals like the Amazon commitment help enable that, he said, because bulk purchasing supports more cost-efficient products.

Hyde specifically asked how much more efficient Amazon’s Graviton chip is for Snowflake’s cost base. Ramaswamy did not give a Graviton efficiency figure. He instead emphasized the broader commercial mechanics: infrastructure scale, customer savings, and the ability for Snowflake and Amazon to go to market together.

Amazon’s side of the arrangement, as Ramaswamy described it, is deeper collaboration around customer problems. He said Amazon is interested in solving customer problems and that a data platform is a key part of that work. Snowflake and Amazon collaborate “at every level of the hierarchy,” he said, including contact between Ramaswamy and Amazon CEO Matt Garman and work between the companies’ teams.

The concrete example was data migration. Ramaswamy described it as a complex problem where tighter Snowflake-Amazon coordination can make the companies more effective together. His summary of the deal was “better together,” meaning more than a procurement commitment even though the $6 billion headline is the most visible part of the agreement.

Snowflake’s productivity case rests on time compression

Snowflake’s claim for customer productivity is that AI reduces the time required to turn data work into usable output. For coding and data work, Ramaswamy said Co-co lets people get jobs done “5 to 10 times faster.” He gave Snowflake’s own data team as an example, saying it had worked through a multi-year backlog in a small number of quarters.

People are literally getting jobs 5 to 10 times faster.

Snowflake Intelligence was presented as a different kind of productivity gain: immediate access to work context. Ramaswamy said that at a conference, before meeting roughly 30 CEOs, he was able in two minutes to know which of them were Snowflake customers and how he should prioritize those meetings. He described that kind of instant access as something that can drive business results.

Ramaswamy’s account of Snowflake Intelligence was that “the entirety of your work” becomes available at a user’s fingertips. In his example, the value was not a new dashboard but quick access to customer context at the moment he needed to act on it. He also cited Nexung as a customer using the products “to great effect.”

M&A is widening what the work agent can see and do

Snowflake’s acquisition strategy is being used to expand the scope of its AI products. Hyde connected that strategy to Ramaswamy’s own path into Snowflake: the company acquired Neeva, the generative AI company he built, after which he became head of AI and later CEO. She also pointed to Natoma, which she characterized as focused on managing data actions of AI agents.

Ramaswamy said Snowflake will remain “very open minded” about M&A. Natoma, in his description, is important because it widens what Snowflake Intelligence can see. The goal is to extend the work agent beyond data already inside Snowflake to other sources that matter to a user, including email, documents and other applications.

That expanded visibility is also meant to support action. Ramaswamy said users can take actions directly from Snowflake Intelligence, not merely ask questions of data. In his framing, acquisitions can add “key pieces of technology” and teams that make Snowflake better, as Neeva did.

The M&A posture fits the broader strategy Ramaswamy laid out: Snowflake is trying to make AI products more useful by connecting data, work context and actions. He presented adoption, cloud scale, pricing changes and acquisitions as related parts of that strategy.