Trump-Xi Summit Puts Rare Earths, AI Chips, and Taiwan at Center Stage

Diet TBPN’s John Coogan and Jordi Hays frame the Trump-Xi summit as a bid for stability shaped by rare earths, advanced chips, Taiwan, and the industrial leaders traveling with Trump. Coogan treats Nvidia chief Jensen Huang’s presence as the clearest pressure point in that diplomacy, while stopping short of fully endorsing the charge that Washington’s AI policy is incoherent. The same search for stability, as the hosts present it, runs into specific limits elsewhere: gated access to Anthropic’s Mythos versus chip negotiations with China, orbital data-center ambitions versus launch and power constraints, and inflation relief versus energy and commodity shocks.

The summit is framed as stability, but the leverage runs through rare earths, chips, and Taiwan

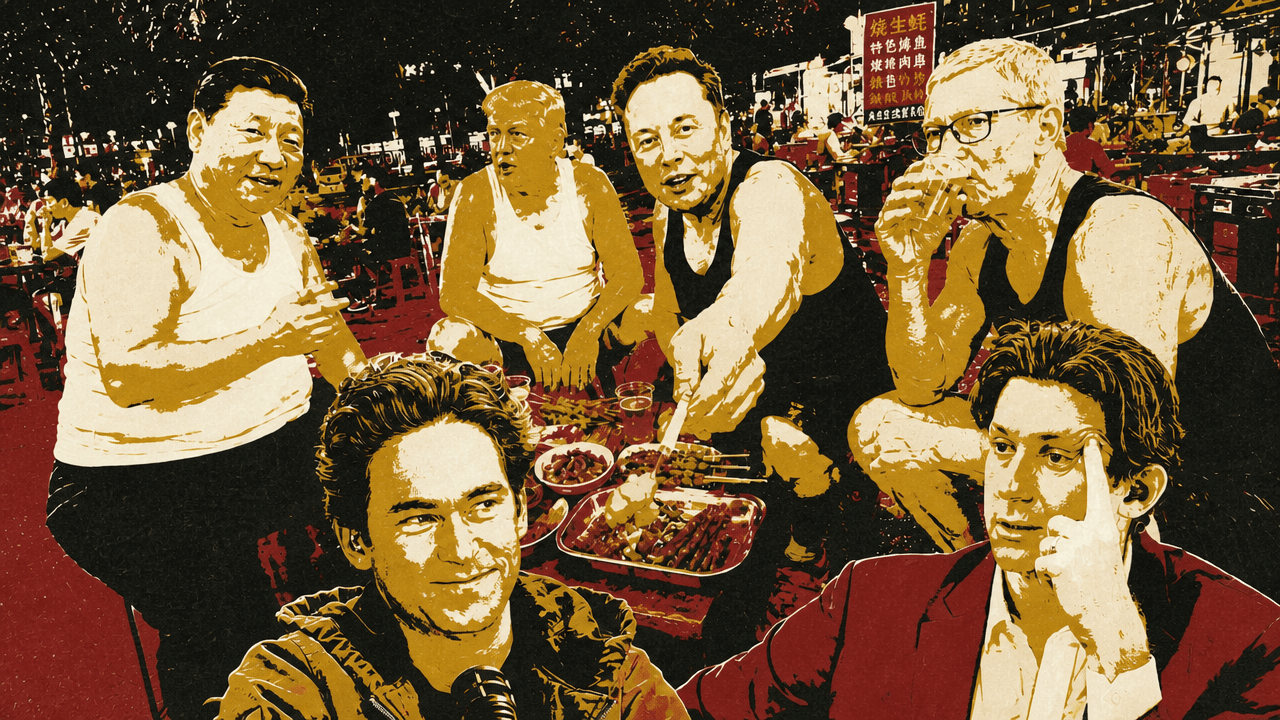

John Coogan treated the Trump-Xi Jinping summit in Beijing as the week’s central geopolitical event, and the business delegation around it as the revealing part. The Wall Street Journal cover he held up framed the meeting as a test of U.S. leverage: “China seeks stability while advancing bigger ambitions.” Coogan’s list of accompanying executives made clear why the diplomatic meeting was also an industrial-policy event: Elon Musk of Tesla, Tim Cook of Apple, Jensen Huang of Nvidia, Kelly Ortberg of Boeing, David Solomon of Goldman Sachs, Stephen Schwarzman of Blackstone, Larry Fink of BlackRock, Jane Fraser of Citi, and Dina Powell McCormick of Meta.

Jensen Huang drew particular attention because Nvidia sits closest to the tension between Chinese access, U.S. export controls, and the AI race. Apple’s China exposure is enormous, Coogan said, but Apple has not been the central focus of chip sanctions in the same way. Nvidia, by contrast, was the company he identified as having “maybe the most tension between the trade deals with China.” Jordi Hays raised the question of whether Huang had always been expected on the trip or was added late after joining in Alaska; Coogan did not offer a firm theory. He pointed instead to the practical difficulty of moving the schedule of “the leader of the biggest company in the world” and to Trump’s post disputing reports that Huang had not been invited.

The symbolism was unusually visible: a post from Disclose.tv showed Trump, Musk, and Huang descending from Air Force One in Beijing, with a guard of honor and flag-waving reception around them. Coogan and Hays spent some time on the theater around the arrival, Air Force One, and Huang’s now-recognizable leather-jacket uniform. The substantive point beneath the aside was simple: Huang’s presence turned Nvidia’s role into a focal point of the trip.

The Wall Street Journal editorial board account that Coogan relayed put the summit’s first-order objective in familiar diplomatic language: the U.S. side wanted stability. On trade, the “best outcome” might be little more than ratifying the status quo — a tariff truce and a promise from Beijing not to use rare earths as a hostage instrument. Coogan’s gloss was that markets and business leaders can adjust to tariffs if the regime is stable. What they cannot absorb as easily is chaos.

Hays pointed out the irony of Trump arriving as the face of stability: “Look guys, all I’m asking for is a little stability.” Coogan tied that back to Trump’s own “stable genius” branding, then returned to the Journal’s more skeptical argument. Xi’s weak economy may create incentives to cooperate, including promises to buy more American farm goods and aircraft, but similar promises had been made before, and U.S. farmers had not regained lost China market share.

Rare earths led directly into chips. In the Journal’s framing, a rare-earths “ransom offer” could become pressure for more U.S. advanced chip exports to China. Coogan said Xi views artificial intelligence as a decisive theater in competition with the United States, and that China is “trailing, though not by much,” perhaps six months by estimates he cited. The administration wants AI guardrails talks with Beijing, but the Journal’s warning, as Coogan presented it, was that AI arms control should not be expected to do much. In that view, the best deterrent is U.S. dominance in models and computing power, not declarations of responsible stewardship.

The concern was not only formal policy. Coogan quoted the Trump administration’s warning that Beijing is engaged in “industrial-scale theft of American AI models,” and referenced a Justice Department indictment involving a technology executive and associates allegedly diverting high-end chips to China. Hays identified the case as Supermicro; Coogan recalled the alleged evasion imagery as shipping labels put on ordinary items such as a hair dryer.

The delegation’s absences mattered too. Musk was present, Huang was present, and Meta had representation through Dina Powell McCormick. But Demis Hassabis and Sundar Pichai from Google and DeepMind were not there, nor were Dario Amodei of Anthropic or Sam Altman of OpenAI. Each has “their own complicated relationships with the federal government and the Trump administration,” Coogan said, so the absence was not shocking. Still, he argued that the lineup suggested a disconnect: Silicon Valley is debating superintelligence, fast takeoff, and U.S.-China AI scenarios, while the highest-level diplomatic conversation may remain focused on semiconductor supply-chain details and export restrictions.

If you were looking for answers to some of the biggest questions posed about how superintelligence will play out in the global stage, the AI 2027 scenario, the China Wakes Up scenario, you’re going to have to keep waiting.

Meta’s presence raised a separate question. Hays said a viewer asked why Meta was there at all, given that Meta platforms have long been banned in China. He suggested the answer might be partly symbolic friendliness and partly the Manus issue, though he emphasized that a $2 billion transaction, if that was the relevant scale, would be a rounding error beside rare earths, oil, aircraft, chips, and Taiwan.

Coogan pushed back only on scale, not on the premise that the issue could matter. In his view, even a single sentence on whether American companies can acquire Chinese companies that have relocated to Singapore, or whether China will restrict the export of talent, whole companies, or technology, would “resound throughout the industry.”

The summit’s deepest risk, in the Journal editorial board’s telling, was Taiwan. Coogan relayed the Journal’s phrase that Xi was setting a “Venus flytrap” for Trump. Xi wants veto power over U.S. arms sales to Taiwan and wants Washington to move from not supporting Taiwanese independence to formally opposing it. Such a verbal shift, presented as minor, would disrupt decades of U.S. policy that had helped preserve peace. Taiwan, Coogan said in agreement with the editorial, is not the aggressor in the Taiwan Strait. The catastrophe to avoid is economic and geopolitical as well as diplomatic.

The broader Journal argument, as Coogan summarized it, was that China remains the main financier and industrial base for “bad actors” from Russia to Iran to North Korea. The first Trump administration understood China as a strategic adversary across military, economic, and ideological dimensions; the second, in the Journal’s phrasing, is searching for détente, with Trump as “the chief dove.” Coogan said that approach has some merit if the U.S. uses the interlude to diversify rare-earth supply chains and pass a $1.5 trillion defense budget to rearm.

Hays added a practical political theory: many people were speculating that significant deals had already been arranged and that the summit was partly ceremonial. If the U.S. president makes a major trip with major industrial leaders and returns without progress, Hays said, the optics become an even larger loss.

Mythos access for Japan exposes an unresolved AI-policy tension

John Coogan connected the summit to a separate development: a tweet containing a screenshot of a Nikkei article said Anthropic had granted Claude Mythos access to three major Japanese banks. The visible screenshot named MUFG Bank, Sumitomo Mitsui Banking Corp., and Mizuho Bank, and said the banks were set to gain access as soon as the end of May. According to the screenshot, the banks were likely informed by U.S. Treasury Secretary Scott Bessent during a meeting in Japan, and it would mark the first time a company from the East Asian nation had been granted access.

The screenshot described Mythos as an AI model that can discover and exploit software security flaws far faster than earlier technology. It also said access had been restricted to roughly 50 corporations and organizations worldwide, including U.S. firms, U.S. banks, and U.K. government organizations. Japan had been pressing Washington for access, according to the same screenshot, and Japanese officials had been focused on finding cybersecurity weaknesses in national infrastructure and minimizing risks posed by advanced AI models.

Coogan then read a criticism from Chris Maguire. Maguire’s argument, as Coogan presented it, was that the Treasury Secretary was personally vetting companies for access to the most advanced U.S. AI model because misuse could threaten national security, while Jensen Huang was flying on Air Force One to Beijing to sell China AI chips that could help it build a Mythos-level model as quickly as possible. The conclusion of that criticism was blunt: the administration’s AI policy is inconsistent and incoherent, and the two approaches cannot be justified simultaneously.

Coogan did not fully endorse the critique. He said he remained sympathetic to the export-control position while also recognizing that a larger negotiation may be underway. But he treated the tension as real. If advanced model access requires case-by-case approval for allies, while advanced chips remain bargaining chips with a strategic competitor, the policy line is difficult to explain cleanly.

The more interesting question for Coogan was what a “Mythos moment” would look like in China. He attributed to Dario Amodei the view that open source and China may be around six months behind Mythos, and said that timeline broadly matches the progress visible from American labs. If that estimate is directionally right, Coogan argued, China will eventually face its own version of the U.S. debate over whether a private AI lab can release or deploy a powerful cyber-capable model, and what authority the state should exercise over it.

In the United States, Coogan said, the Mythos moment produced a confrontation involving Anthropic, the Department of War, Dario Amodei, and Emil Michael, including threats of a supply-chain designation. Coogan said that designation “doesn’t feel like” it went anywhere, because Anthropic’s business is still operating, Mythos is available through hyperscaler clouds, and the model is being granted to Japan. Still, in his account, the episode forced debate over what rules should govern frontier AI and what authority should rest with private companies versus the government. America handled that in what Coogan called a “democratic way, loosely”: evaluating the technology, considering stronger state intervention, and debating the bounds of government power.

China’s version, he suggested, would be structurally different. Coogan said Chinese tech companies that become very large often appear to face pressure from the CCP. He described DeepSeek’s parent company, High-Flyer, as unusually positioned because, in his understanding, the founder has an immense amount of control. Hays added that the founder had invested $2 billion of his own money into what Hays characterized as a low-dilution round.

Coogan contrasted that with Anthropic, where Amodei had many co-founders, substantial dilution from funding rounds, and a broad cap table. Anthropic, he said, is moving like a typical American company with many stakeholders and perhaps a future public-company path, which would bring more SEC oversight.

That leaves a different question for China: what happens if a closely held private company with comparable AI capabilities operates under a more aggressive state? Coogan said there is some evidence China may be on a shallower growth trajectory, but even if Amodei’s six-month estimate stretches to a year, “something is going to happen there.” China will have its own Mythos moment, he argued, and what the rest of the world learns about it may be dramatic.

Tyler Cosgrove was more cautious. He pointed to graphs suggesting open source is increasingly falling farther away from frontier models, and said it is hard to know what is actually happening in China. The key unknown is not simply capability but governance: what does it look like, in practice, when the CCP begins exerting more control over an AI company?

Coogan sharpened that into an infrastructure question rather than an answer. If China needs to consolidate the Blackwell-class chips entering the country into one networked data center capable of training a Mythos-level model, he asked, can it continue to be pro-competition? The question was not only whether China can obtain enough compute, but whether its political and industrial system would centralize that compute when frontier training demands it.

Space data centers are still constrained by power, cooling, and launch cost

Jordi Hays said SpaceX and Google are in talks over launching data centers into orbit. The on-screen title card, attributed to the Wall Street Journal, summarized the constraint set plainly: “Power, cooling, launch costs still key questions.” The potential deal would connect two companies that may also compete in orbital data centers: SpaceX, whose CEO Elon Musk has described space compute as the next frontier for his rocket company, and Google, which is expanding its own effort.

Hays said Google is also in discussions with other rocket launch companies, which he interpreted as a “stalking horse” dynamic. The technology remains unproven, but it has become part of the strategic imagination around compute infrastructure.

John Coogan responded by pushing the premise into other speculative geographies. If space data centers are on the table, why not blimp data centers? Sergey Brin has a blimp company, he noted. Bezos has Blue Origin, creating an imagined path from AWS to space-based compute. Coogan’s joke rested on one of the same pressures behind the orbital idea: terrestrial data-center siting can run into political and permitting objections. “There’s no NIMBYism in the middle of the Pacific Ocean,” he said, if data centers are floating in circles.

Tyler Cosgrove extended the bit underwater: if the ocean is available, why not go down instead of up? Underwater data centers would have “Atlantis, max cooling” advantages. Coogan said the bottom of the ocean feels easier than space in some respects because cooling is available; energy is the difficult part. Tyler suggested geothermal. Hays suggested oil and natural gas reserves on the seafloor, before Tyler asked the practical combustion question: how do you burn oil and gas underwater without oxygen?

The exchange was comic rather than a developed infrastructure proposal. But it kept circling the same constraints named in the Journal frame. Space data centers promise a way around some terrestrial limits, yet still have to answer launch cost, power, cooling, maintenance, and operations questions.

Hays said the speculative technology has been at the center of SpaceX’s pitch to investors ahead of its planned IPO this summer, which the Journal report, as Hays relayed it, anticipated could be the largest IPO of all time. Google, meanwhile, had announced plans the previous year to launch prototype satellites by 2027 under a moonshot initiative called Project Sun Catcher, working with Planet Labs. Hays quoted Sundar Pichai’s description of starting with tiny racks of machines in satellites, testing them, and scaling from there.

The striking part was Pichai’s timeline. Hays quoted him saying that “a decade or so away” orbital data centers could be viewed as a more normal way to build data centers. Coogan immediately contrasted that caution with Musk-like acceleration: “Elon’s like, I thought we were 10 days!” Hays agreed that Pichai’s wording was deliberately careful.

Coogan also said Google was an early investor in SpaceX and owns 6.1% of the company. He then drew a broader point about the increasingly tangled web of technology ownership. In his telling, the OpenAI Startup Fund had invested early in Cursor, and because of later dealmaking, OpenAI or its startup fund could have meaningful exposure to SpaceX. Coogan imagined the headline language: “OpenAI-backed SpaceX IPO.” His conclusion was that everyone increasingly owns pieces of everything else.

Inflation anxiety returns through energy, aluminum, and bond-market expectations

John Coogan turned to the financial story running alongside the geopolitical and AI narratives: inflation had accelerated. He said inflation was up 3.8% last month and pointed to a Joe Weisenthal post reacting to producer prices. Weisenthal’s post, shown on screen, said simply “man” above the headline: “US April Producer Prices Rise 6.0% Y/Y; Est. +4.8%.”

Coogan attributed the pressure partly to the closure of the Strait of Hormuz. His concrete example was Diet Coke. Caffeine and flavoring may not come from the Middle East, he said, but aluminum does have Middle Eastern smelting exposure. If aluminum supply tightens because of the Strait closure, cans become a constraint, and Diet Coke can go out of stock. Hays joked that Coogan had four or five pallets; Coogan said he had not yet begun stockpiling.

The larger issue was investor expectations. Coogan said surging energy prices had pushed inflation expectations to multi-year highs, and that a hot CPI reading intensified Wall Street anxiety. Stocks, he said, had largely shrugged off the U.S.-Iran conflict and resulting energy shock, but inflation expectations were a potential trouble spot.

A Federal Reserve Bank of St. Louis chart compared the five-year break-even rate with the five-year TIPS yield from 2020 through 2025. Coogan explained the mechanism: investors express inflation expectations through ordinary U.S. Treasuries and Treasury Inflation-Protected Securities. The gap between those yields, the break-even rate, had recently reached its highest level since October 2022, implying that investors expected annual inflation to average about 2.7% over the next five years.

Coogan said that figure was not “entirely doom and gloom.” But the risk, in his view, is distribution. If headline GDP strength is concentrated in AI capex and data centers while the broader real economy grows only 0.1%, then 2.7% inflation over five years becomes a stagflation setup. He defined the concern plainly: stagnation plus inflation, “a very rough thing for any economy to go through.”

Jordi Hays framed the monetary-policy handoff sympathetically. Whatever history says about Jerome Powell, Hays said, he “landed the plane,” only for war in the Middle East to reintroduce inflation pressure. If Kevin Warsh were to take over, Hays suggested, he could inherit an equally difficult job.