Overlooked Distribution Channels Power Three Eight-Figure Businesses

Sam Parr and Shaan Puri use three founder interviews to make a case that overlooked distribution channels can support large, durable businesses. The examples are Haven Lifestyles, a $10 million real-estate advertising company built on mailed magazines; Team Outsider, a roughly $20 million campground operator built through succession deals with family owners; and Autopilot, a $30 million gross marketplace business that lets retail investors follow politicians, hedge funds and vetted stock pickers from their own brokerage accounts. The argument is that the edge in each company came less from novelty than from treating neglected channels — postal routes, campground relationships and public financial filings — as the core of the business.

Overlooked distribution was the business model

The three companies were not interesting because they were odd. They were interesting because each founder found a distribution system many ambitious founders would not normally treat as a company-building platform.

Haven Lifestyles uses postal routes, real-estate-agent budgets, outsourced design, online amplification, and AI-assisted sales follow-up to turn unsolicited magazines into a $10 million advertising business. Team Outsider uses handwritten letters, cold calls, long seller relationships, real-estate financing, and hospitality operations to buy family-owned campgrounds before the owners’ succession problem becomes someone else’s deal. Autopilot uses public financial disclosures, brokerage integrations, and creator-marketplace economics to let retail investors follow politicians, hedge funds, and independent stock pickers without handing over custody of their assets.

The revenue numbers were the entry point. Alex Daniels said Haven Lifestyles owns 40 real-estate advertising publications and does $10 million in revenue. Josh Weissenstein said Team Outsider owns 16 campgrounds across 10 states and expects about $20 million of revenue this year. The Autopilot founder said the company has about $30 million of gross marketplace revenue, roughly $22 million of Autopilot ARR, 30 to 35 employees, and venture firms have floated Series B valuations in the $300 million to $400 million range.

| Company | Revenue cited | Core channel | Main bottleneck | Proposed lever |

|---|---|---|---|---|

| Haven Lifestyles | $10M revenue; about $2.5M profit | Postal-route real-estate magazines plus online distribution | Agents buy once around a listing, then drop off | Improve retention by calling top customers, deepening relationships, and getting existing agents to advertise one more time |

| Team Outsider | About $20M expected revenue this year | Long-term succession relationships with family campground owners | Scaling hospitality culture across hourly teams in 10 states | Study frontline-service companies and import proven operating systems and incentives |

| Autopilot | About $30M gross marketplace revenue; about $22M ARR | Public filings, verified portfolios, and brokerage-connected copy trading | Hiring senior talent fast without lowering the bar | Define roles precisely, use outside interview calibration, and recruit from proven operators plus high-upside generalists |

The shared pattern was specific. Homeowners can still be reached through local real-estate mail. Family campground owners still need a trusted successor when their children do not want the business. Retail investors still want to know what successful traders, politicians, hedge funds, and stock pickers are buying. Each company turned one of those existing behaviors into a channel.

Shaan Puri captured the point after hearing the businesses: these were “three ideas that didn’t even exist” in his cone of vision. That was less a comment about novelty than about blind spots. Postal mail, campground succession, and investment filings can all become acquisition channels if the operator understands the niche well enough.

Autopilot turns public financial signals into a marketplace

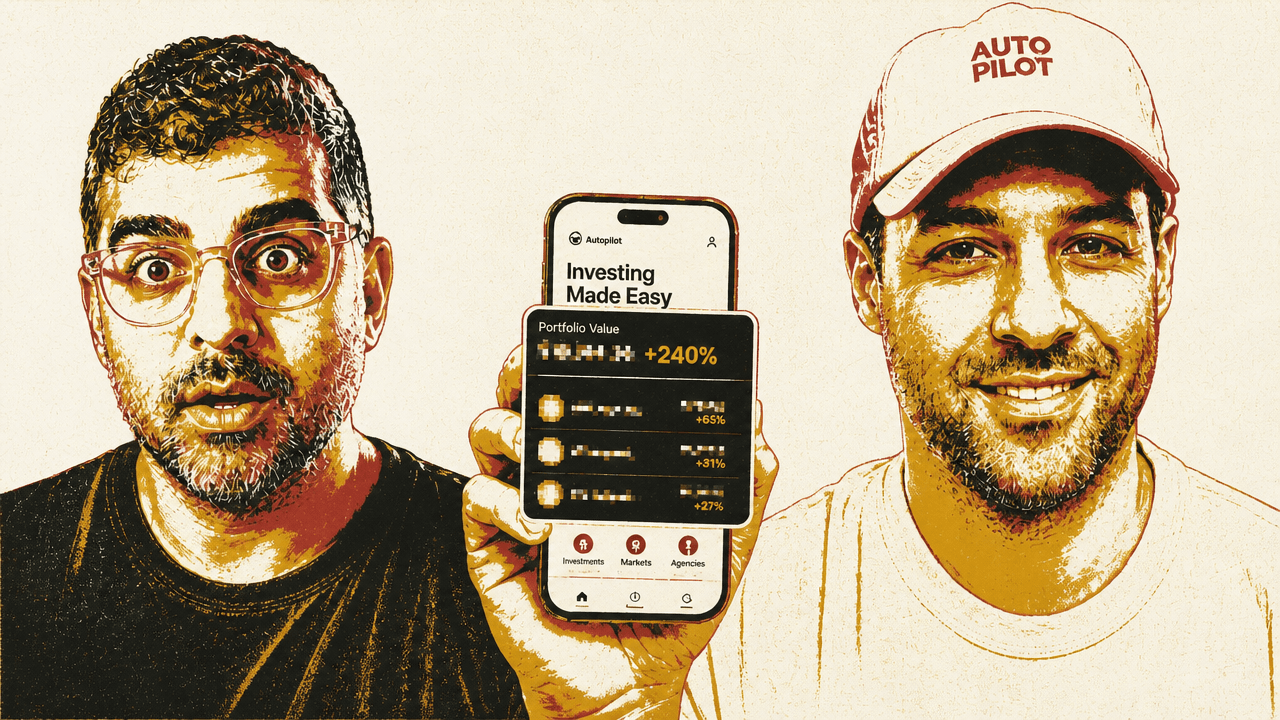

Autopilot was the most venture-shaped company in the group: an app that lets users invest by following politicians, hedge funds, and vetted portfolio creators. Its core premise is simple. A user connects a brokerage account, such as Robinhood, chooses a portfolio to follow, and Autopilot sends trade instructions to the brokerage when that portfolio changes. The user’s money stays in the user’s brokerage account.

The founder treated that custody distinction as central. Users do not give money to the pilot or to a fund manager, he said. They keep assets in their own brokerage account, which he described as important to how Autopilot can operate from a legal standpoint. Once a company takes custody of assets, he said, the SEC and brokerage-related regulation become much more involved.

Autopilot began as a company called Iris six years earlier. The idea was to let people see into other people’s portfolios. Autopilot itself has been operating for three years. The founder described the business as cash-flow positive, though not GAAP profitable, and said it is growing about 250%. He also said the company is on track, though with difficulty, to reach $100 million in revenue by March of the following year.

The company’s first marketplace problem was supply. In a two-sided marketplace, the founder said, if there is no one good to follow, users will not come; but if there are no users, good portfolio creators have little reason to launch. Autopilot’s answer was to “manufacture the supply side” using publicly available information.

The most visible example is the Pelosi portfolio. The founder said Autopilot built a portfolio around Nancy Pelosi’s publicly disclosed trades and owns that portfolio itself, which means the company keeps 100% of the revenue. Asked whether Pelosi hates Autopilot, he said “probably,” though he added that she had not sent a cease and desist. He joked that when she retires, the company would like her to join the fund and appear in a commercial.

The public-disclosure strategy gave Autopilot a marketing hook as well as a product wedge. The company sponsored a UFC event before the election with “Invest like a politician” messaging, hired a Nancy Pelosi lookalike, bought her a front-row ticket, and wrapped a Cybertruck with “PELOSI 2024” and Autopilot branding. On screen, a vertical social video showed the lookalike arriving in the Cybertruck, mingling at the UFC event, Autopilot app screens, and a headline reading: “Trading app goes viral thanks to ‘Nancy Pelosi’ lookalike at UFC match.” The visible captions framed the product as an app where users “pick who you want to follow” and copy the portfolio that person follows.

The founder said the front-row ticket cost $60,000 and the total marketing buy was about $450,000. It did not help directly, he said, and he probably would not do it again. The intended earned-media moment was Donald Trump sitting near the ring while “Invest like a politician” and the Pelosi lookalike were visible. Trump did not attend that weekend after an assassination attempt. The founder still treated the stunt as evidence that unusual, over-the-top marketing can create attention that remains useful long after the campaign.

That public-portfolio wedge is now being joined by creator portfolios. Autopilot calls its portfolio creators “pilots.” A pilot can set a subscription price, usually from $100 to $500 per year, and users pay to follow. The founder said the top pilots make around $1 million to $2 million per year on Autopilot, separate from any gains in their own portfolios. One pilot, Peter Wolff, has about $220 million following him on the platform, according to the founder.

Wolff illustrated how Autopilot vets supply. The founder said he initially checked Wolff’s personal Robinhood account over a video call and saw that Wolff was up 200% over three years. He acknowledged three years is a short period and raised the question of how a strategy behaves in a downturn, but said he liked how Wolff thought about hedging risk. Autopilot now has technology that can connect to and automatically analyze a brokerage account.

Puri described the company as “picking the pickers.” The founder agreed. Autopilot looks at track records, actual portfolios, and the fit between a creator’s public investing content and the creator’s real holdings. He said there is a 6,000-person waitlist to launch a portfolio on the platform. If a newsletter writer has persuasive public stock picks but a poor actual portfolio, the company does not want that person on the platform.

That is the product’s distinction from stock-picking media. A newsletter can publish a convincing thesis, point to the last winner, and avoid emphasizing the losing calls. Autopilot’s promise, as the founder framed it, is that users can see winners, losers, full performance, dollars following, and the creator’s content. Puri noted that this transparency could reduce the number of financial influencers because it becomes clearer who is legitimate and who is not.

The founder’s ambition is much larger than creator subscriptions. He said Autopilot’s goal is to become the world’s largest asset manager. His institutional analogy was BlackRock Aladdin, which he described as a tool financial institutions and companies use to buy portfolios and manage exposures. He said Aladdin makes around $6 billion per year. Autopilot, in his framing, is trying to build analogous technology for retail investors: for example, a Facebook employee could use Autopilot to find a portfolio designed to hedge tech exposure.

The company also tracks hedge-fund filings. The founder said users can follow the top 15 picks of “Leopold” based on 13F filings, with about a 45-day lag. In the discussion, Leopold was described as a former OpenAI employee who started a fund, raised substantial capital, and made large gains by identifying AI infrastructure bottlenecks beyond GPUs, including SSDs and Micron. The founder said a fund needs $100 million before the filings apply. The hosts treated the example mainly as evidence that a new generation of investors can build public reputations through strong theses and visible results.

The risk is that Autopilot’s three years have been strong years. Sam Parr pressed on what happens after three bad market years. The founder answered that retail investors now persevere longer than they used to, though he acknowledged that a sustained downturn would raise broader questions. Parr compared the risk to Robinhood’s near-death moment during the GameStop period. The founder said Robinhood had to raise about $4 billion immediately, while also saying he was not fully familiar with the DTCC mechanics.

Autopilot also has an unusually concentrated founder alignment story. When Parr asked where the founder’s liquid net worth was allocated, he said roughly 90% of his net worth was “on Autopilot,” much of it in Autopilot equity. The platform also verifies “skin in the game” for pilots, showing how much of their own money follows their own portfolios. The founder gave Wolff as an example, saying Autopilot can show that Wolff has $500,000 following his own trades.

Haven treats the mailbox as paid media

Alex Daniels described Haven Lifestyles as a real-estate advertising company built around magazines, not as a subscriber publication. Real-estate agents pay Haven to promote listings. Haven packages those listings into local or regional lookbooks, prints magazines of roughly 100 to 200 pages, and mails them to households selected by factors such as property value and income. The same content is also distributed online, where Daniels said most exposure now comes from.

The company has divided the United States and Canada into 40 zones. It prints 30 different magazines a month, with each publication on a six-week cycle. Daniels said Haven mails about half a million magazines a year, has 20 employees, and produces about $10 million in revenue with roughly $2.5 million in profit.

The customer is the agent. The household receives the magazine, but the agent pays for the ad. Daniels said agents use Haven both to sell current listings and to win future listings by telling homeowners their property will be advertised. Parr pushed on whether the product was really a magazine or a brochure. Daniels insisted it was a magazine. Parr called it “junk mail.” Daniels conceded it is not subscriber-driven, but emphasized the online distribution that now accompanies the mailed copies.

The on-screen Haven material made the product’s positioning clear. Haven’s homepage featured luxury real-estate content and property images, including headlines about turnkey demand among California buyers, West Coast luxury, AI changing home marketing, and luxury golf communities. Another visual showed a grid of Haven digital magazine covers, all styled as glossy real-estate publications. The business sells the perception of premium editorial packaging even though the revenue mechanism is paid listing promotion.

Daniels’s path into the business came through sales, not media. He had worked as a bill collector for about five years through and after college, calling people about credit-card debt, including Victoria’s Secret credit cards. He said that experience helped him because it trained him to ask for money and absorb rejection. After an HR dispute at that job, he texted his college roommate Ryan about starting something. Ryan had a small publication in Annapolis, Maryland, and agents had asked whether he could launch something similar in Washington, D.C. They launched there.

Year one produced about $300,000 in revenue. The early sales motion was direct and physical: create a free version of the magazine, show agents what it would look like, then meet them in person. Daniels said the first meeting produced a yes. Another prospect asked what $10,000 would buy, far more than they were charging. Daniels kept calling his business partner between meetings to report another sale, but kept his existing job for eight months.

The operational system is plain. Haven handles the artwork for advertisers, using designers largely in the Philippines. It buys postal distribution through the post office by selecting routes, and it has to keep magazines within certain dimensions and weight limits to avoid cost problems. Puri compared the post office to Facebook ads: a distribution system that sells access to attention and addresses. Parr summarized the point as “the post office is basically Facebook ads.”

The most useful growth discussion was not about launching more magazines. Daniels said Haven could break its 40 zones into smaller markets, because some editions currently combine entire states or less attractive markets. A more granular edition might resonate better locally. He also saw opportunities in adjacent verticals beyond real-estate agents.

Parr’s strongest instinct was home services. If Haven can help agents sell to homeowners, a home-services publication could potentially help roofers, landscapers, HVAC companies, and other providers reach the same households. Puri argued that a home-services version should not just be a directory of vendors. It should lead with genuinely useful homeowner content — for example, a seasonal cover story with “five tips every homeowner should do” before winter — and then include providers for readers who would rather hire help.

Puri’s broader advice was to study the category more aggressively. Daniels did not have a clear map of the biggest players in adjacent mailed-publication businesses, and he acknowledged that as a weakness. Puri recommended reverse-engineering companies that use mailed magazines or informational products to build large advertising businesses: identify who is big, who used to work there, what the model looks like, and what transferable lessons exist. Neighborhood publications such as Stroll came up as a relevant comparison. Daniels said those companies were “definitely over 100 million.”

The immediate profit lever, however, was retention. Daniels said Haven works with more than 10,000 agents a year, but many advertise only when they have a major listing and then disappear. About 1,500 customers are on annual auto-debit plans. Daniels said the easiest way to double profits would be to get existing advertisers to advertise one more time.

Parr asked how many of those agents Daniels had personally spoken with that year. Daniels said zero. The prescription was straightforward: call the top 100 spenders, not necessarily to sell, but to understand why they buy, why they do not buy more, what they love, and what they hate. Nothing bad is likely to happen from talking to the best customers; a lot of good can happen.

Puri added a relationship-scoring framework he had seen a CEO use. Tier 1 customers are on texting terms and would do a favor quickly. Tier 2 customers are friendly email relationships. Tier 3 customers are transactional. Tier 4 is weaker still. Applied to Haven’s top 100 customers, the exercise would show whether the company has deep relationships with the accounts that matter most or merely recurring transactions.

The company is already using automation to support the sales process. Parr said the founder of Lindy had called Daniels’s AI setup one of the most impressive he had seen. Daniels said Haven uses Lindy to respond to inbound emails, follow up, upsell, and move prospects through the sales flow. Haven still has salespeople, but their work has shifted toward customer experience and getting advertisers to return.

People underrate how much of entrepreneurship is psychological and not strategic.

Daniels said his real goal is not necessarily to reach $100 million in revenue, but to double profit. He had recently set a target to double profit run rate within a year, leaving 11 months at the time of the discussion. Puri pushed the psychological dimension: what would change if Daniels decided that 25% net margins had to become 35% within six months? His view was that once the goal became specific and non-negotiable, the answers would likely become more obvious.

Team Outsider buys the moment when a family needs a successor

Josh Weissenstein described Team Outsider as a company that acquires family-owned campgrounds, usually from owners looking to retire. The company has 16 campgrounds, about 4,000 sites, operates in 10 states, and expects about $20 million in revenue this year. Weissenstein said it has raised around $60 million and owns assets worth north of $100 million.

A campground, in his explanation, is closer to an outdoors hotel than to an empty piece of land. Guests rent RV pads, tent spaces, or cabins. The properties often include stores, cafes, ice cream, burgers, pizza, swimming pools, lakes, and, in one case, a go-kart track. The on-screen Team Outsider homepage showed a grid of KOA campgrounds and RV resorts across states including Ohio, New York, Wyoming, Kentucky, Wisconsin, Illinois, and Virginia, with guest-review snippets and “Visit” buttons. Another visual showed Neversink River Resort, including cabins, an Airstream trailer, and a property map.

Team Outsider’s thesis combined hospitality, real estate, fragmentation, operational complexity, and emotional meaning. Weissenstein and his partner Cody met in college, started an unsuccessful business together, stayed friends, and later decided to work together again. They were non-technical founders looking for a market large enough to support a company, fragmented enough to consolidate, complex enough for an operator to create value, and meaningful enough that employees and customers would care.

Puri asked for the less polished version of the origin story. Weissenstein said their backgrounds were in hospitality and real estate, and Cody lived in Bozeman, Montana and was an avid RVer. Cody suggested that Weissenstein fly from New York to Montana so they could drive around, meet owners, team members, and guests, and test whether the market had “a spark.” Weissenstein said he fell in love with the space.

The first deal shows the acquisition model. Team Outsider bought an existing operating campground near Yellowstone for about $3 million. It was generating roughly $500,000 of top-line income and about 35% cash flow, or approximately $150,000. The purchase used an SBA loan for more than 80% of the price, with the rest in cash. A few years later, Team Outsider had increased NOI to close to $300,000, refinanced, taken out its cash, and used that capital to buy the next property.

| Metric | First campground at acquisition | After improvements |

|---|---|---|

| Purchase price | About $3M | — |

| Revenue | About $500K | — |

| Cash flow / NOI | About $150K | Closer to $300K |

| Financing | 80%+ SBA loan | Refinanced and took cash out |

The improvement playbook is not exotic. Many acquired properties have been run for decades by families and lack digital marketing, modern websites, digital reservation systems, VoIP phone systems, review management, and standardized training. Team Outsider installs those systems and professionalizes the operations.

The hard part is not only operational. It is relational. Weissenstein said Team Outsider is often the succession plan for owners whose children do not want the business. These sellers are not merely selling land or cash flow. They have often served guests personally for decades, and many guests are effectively friends. One seller relationship had been in progress for five years before a deal. The objective is to be trusted enough that, when the owner is ready, Team Outsider gets the call.

That reality shapes sourcing. The company writes handwritten letters, makes cold calls, follows up, and tries to catch owners at the right time. During season, many owners are behind the front desk and exhausted. There are Facebook groups, conventions, and industry channels, but Weissenstein said the space also has mistrust toward being overmarketed. The challenge is to become visible without seeming inauthentic.

The real-estate case for campgrounds rests on strong yield, operational complexity, and tax characteristics. Weissenstein said complexity creates opportunity to drive value. He also said the depreciation characteristics can be attractive, similar to manufactured housing, because roads and infrastructure can be depreciated while many rural properties have limited land and building value.

The company originally thought it might use third-party property managers after learning the business. Cody managed the first location himself for a year, including scrubbing toilets and doing the hands-on work. But Team Outsider concluded that it could not outsource culture and that, at least at the time, there were not third-party managers capable of scaling with it. The company built its own operating company instead.

That choice makes Team Outsider less like passive real estate and more like a hospitality company. Weissenstein said the business has tens of thousands of guests every year and about 350 team members. Puri noted that many real-estate investors choose real estate for flexibility and cash flow; Weissenstein is building a company. Weissenstein agreed, adding that it is also a hospitality business.

The hospitality problem became his central operating question: how to scale culture across hourly employees in 10 states and keep people incentivized to deliver high service. Puri pointed to companies that have already solved analogous frontline-labor problems. From his own restaurant-business experience, he recalled the founder of Chipotle saying that getting frontline workers to care about customers the way founders care about the first location could create a huge business, but is one of the hardest things to do. Puri said Chipotle used incentives and career ladders, including payments to managers when employees they developed later became general managers.

The practical advice was to study 15 companies that have solved similar problems, identify common patterns, and hire or consult people who were present during the relevant scaling phase. A retired executive from a cruise line or hospitality company may not want a full-time job, but may have exactly the operating knowledge Team Outsider needs.

Parr added two examples from Will Guidara’s “unreasonable hospitality” approach. In one, a Ford dealer found a forgotten customer moment by placing a $15 Starbucks gift card in the glove box of every car with a note meant to surprise the buyer. In another, a UPS store owner ran a weekly contest where the employee who delivered the most hospitable act won $20. Parr’s point was that small incentives and recognition can redirect what frontline workers compete over.

Weissenstein said most employees are aligned with the company’s mission “to be the most hospitable team in the world,” which matters because replacing family operators is hard. But outliers happen. One employee turned out to be a convicted bank robber who had robbed nine banks, and Weissenstein had to fire him in person in the middle of nowhere. In another case, guests alerted the company that employees had been cutting down trees and selling the wood for cash on Facebook.

The long-term thesis extends beyond campgrounds but starts there. As more of life moves online, Weissenstein believes businesses that bring people together in the real world will become more valuable. Campgrounds still have runway, and Team Outsider still has a pipeline of properties it wants to own. He said he hopes to keep doing it indefinitely.

The bottlenecks were managerial, not conceptual

The clearest operating lesson across the three companies was that the idea was not the hardest part. Each founder understood the basic opportunity. The constraints were more specific: customer retention at Haven, culture at Team Outsider, and senior hiring at Autopilot.

Alex Daniels did not need to prove that agents would buy ads. More than 10,000 agents already work with Haven each year. His problem was getting them to buy more often. That makes customer intimacy a profit lever, not a soft exercise. The top 100 customers should reveal what repeat purchase actually depends on: whether the product produces measurable value, whether agents forget, whether sales follow-up is wrong, whether annual plans are underused, or whether the company is missing a higher-value packaging model.

Josh Weissenstein had the opposite problem from automation. Team Outsider can install websites, reservation systems, phones, and marketing, but its promise to sellers and guests depends on service quality. It is replacing mom-and-pop operators whose advantage was personal care. The company therefore has to build systems that make hourly workers act with ownership across many locations.

The Autopilot founder’s bottleneck was senior talent. He said polished senior candidates can sometimes “BS” better than he can detect it. Sam Parr’s answer was to use outsiders when hiring for roles the founder does not fully understand. An outside hiring committee can test for expertise and pattern-match against what excellence should look like.

Shaan Puri’s answer began earlier, with the job definition. Many hiring mistakes start because the founder is not clear enough about what the role is meant to change. A generic job spec outsourced to a recruiter or ChatGPT attracts generic candidates. The founder needs to write down the actual problem, what the person must be world-class at, and what they must accomplish inside the company.

Puri also described using a friend who was better at hiring as a calibration mechanism. For executive searches, he would screen candidates, then ask the friend to interview the top three or four. The value was not simply the friend’s final recommendation. It was watching how the friend challenged answers, dug past first responses, and detected weakness. That made Puri a better interviewer.

His hiring framework had two main talent pools. The first is people who have already solved the exact problem before. Not people who merely worked at a successful company, but people who were present at the right stage, on the right problem, and actually drove the result. The second is unproven “diamonds in the rough” — people who have not done the job before but look like unusually high-upside generalists. Puri said companies should build systems to source consistently from both pools.

Parr agreed with the bias toward proven experience. Hiring young, inexperienced people can be fun, especially for founders who recently were young and inexperienced themselves. But “you did that there, do that same thing here” tends to work far more often.

The Autopilot founder said he spends about 20% of his week recruiting, roughly a full day. Puri said that is already better than many founders with hiring problems, who often cannot say how many hours they spend. The founder said he had come to see recruiting as central and had heard that many successful founders in scaling phases spend more than 30% of their time on it.

Autopilot is hiring engineers, product people, growth people, marketing people, and “really anyone” who clears the bar. It is hiring only in New York. The founder said the company can afford expensive talent and had recently offered someone a $350,000 salary, which felt strange to him because he had never made that much himself and still does not. His justification was that with AI, a strong person can be 10 or 20 times more effective than an average person.

Puri reinforced that standard with a phrase from a former CTO: “You’re one person? No, you’re three people.” The idea was not literal headcount replacement, but a bar for resourcefulness: avoid low-value work, automate what can be automated, find faster paths, and produce at a higher rate. At offsites, Puri said, they used the phrase “every day is two days” to set the tempo.

The Autopilot founder also described a hard-edged performance culture. If new hires arrive and do not produce anything meaningful within two or three weeks, he said he is quick to let them go. Parr noted that this affects culture and makes hiring accuracy even more important. The founder said employees are told that if they last more than three months, they do not need to worry; before that, people are “freaked out.”

The pattern is useful because it keeps the word “execution” from becoming vague. At Haven, execution means increasing repeat purchase from agents the company already has. At Team Outsider, execution means translating family-style hospitality into systems hourly workers can repeat. At Autopilot, execution means hiring fast enough for a venture-scale marketplace without letting impressive candidates lower the talent bar.

The edge came from knowing where others do not look

Each company was built around an existing behavior. Real-estate agents already spend money to market themselves and their listings. Campground owners already need a way to retire without betraying the guests and communities they have served for decades. Retail investors already look for signals from politicians, hedge funds, newsletters, and unusually successful stock pickers.

Haven made mailed real-estate advertising feel like a premium magazine and supported it with design operations, postal-route targeting, online traffic, AI-assisted sales follow-up, and advertiser retention. Team Outsider made campground succession investable by combining relationship sourcing, SBA and outside capital, in-house operations, and hospitality culture. Autopilot made copy-trading legible as a consumer marketplace by turning public disclosures and verified creator portfolios into followable products inside a user’s own brokerage account.

The hosts’ reactions were partly admiration and partly diagnosis. Sam Parr admired Daniels’s calm and said he wanted to “steal” that trait without necessarily trading lives. Shaan Puri saw both sides of Daniels not being in a rush: “for better and for worse, but mostly for better.” Weissenstein’s business sounded idyllic from a distance, but the actual work involved weekly travel, hundreds of employees, exhausted sellers, and frontline hospitality. Autopilot’s metrics were the most venture-scale, but its risk profile included regulation, market cycles, high-velocity hiring, and the challenge of proving that users stay when portfolios stop going up.

What made the businesses notable was not that they were easy. It was that they sat in places many founders do not bother to study: the mailbox, the campground front desk, the public filing, the agent follow-up cycle, the handwritten seller letter, the UFC stunt, the 45-day-lagged hedge-fund position.

Those are not glamorous channels. They are channels. And in each case, the operator’s advantage came from treating an overlooked channel as the center of the business rather than as an afterthought.