Nvidia Says AI Demand Is Expanding Beyond Hyperscale Cloud Buyers

Bloomberg’s Neil Campling said Nvidia’s latest quarter showed both the strength and the constraint of the AI trade: revenue beat estimates sharply, but expectations and index positioning left limited room for a larger stock reaction. His main point was that Nvidia is trying to shift investor attention from competition in hyperscaler chips to a broader AI infrastructure market spanning agentic AI, physical AI, sovereign AI and fast-growing AI companies. In Campling’s account, Jensen Huang framed that opportunity as potentially reaching $3 trillion to $4 trillion in annual infrastructure spending by the end of the decade.

An 85% growth quarter still met a positioning problem

Neil Campling framed Nvidia’s latest results as a tension between exceptional reported growth and a market that had already priced in much of the story. On the face of it, he said, 85% top-line growth was “quite stunning.” He also described it as the company’s 15th consecutive quarter beating both top-line expectations and guidance expectations. But expectations going into the result were already high, which helped explain why the stock reaction was muted.

Two numbers anchored the discussion: Bloomberg’s revenue table showed total fiscal first-quarter 2027 segment revenue of $81.6 billion, 11.4% above estimates; Campling also said Jensen Huang had talked about AI infrastructure spending reaching as much as $3 trillion to $4 trillion a year by the end of the decade. The first number explained the scale of Nvidia’s current beat. The second explained why Nvidia is trying to move the debate beyond whether hyperscalers have alternative chip options.

| Segment | Fiscal 1Q 2027 revenue | Versus estimate |

|---|---|---|

| Compute | $60.4B | -1.1% |

| Networking | $14.8B | +16.1% |

| Edge computing | $6.4B | +13.1% |

| Total | $81.6B | +11.4% |

The table sharpened the point. Compute remained by far the largest line at $60.4 billion, but it was shown 1.1% below estimates. Networking, at $14.8 billion, was 16.1% above estimates. Edge computing was shown at $6.4 billion, 13.1% above estimates, with Bloomberg noting that this was an aggregate of estimates for other business lines. Total segment revenue, however, was well ahead of estimates.

Campling’s explanation for the muted stock reaction was positioning rather than disappointment with the quarter. Nvidia is already a large part of the US technology market and a major component of the index, he said, making it harder to see where substantial incremental buying would come from. In his view, investor enthusiasm was showing up more clearly in other parts of the AI ecosystem, including Asian stocks that had already moved that morning.

The result was strong, but it landed in a market that had expected strength. Campling’s point was that Nvidia’s own numbers were only one part of the market reaction; ownership, index weight and prior expectations also mattered.

Competition in hyperscaler chips is being answered with a bigger market

Neil Campling acknowledged competition from other chipsets in the hyperscaler market. The response he emphasized was not a product-by-product defense of Nvidia’s position inside that market. It was the larger opportunity set Nvidia is trying to describe to investors.

Huang, in Campling’s account of the call, talked about agentic AI and the potential for physical AI. The call also included a comparison between the growth of OpenAI and Anthropic and the earlier software-as-a-service era: those AI companies, Campling said, are reaching in a month what took SaaS companies up to a decade to reach. He called that pace “quite phenomenal.”

Huang also said, according to Campling, that “a hundred trillion dollars of industry” was about to be affected by AI. That was the basis for the broader framing: even if hyperscalers have alternative chip solutions, Nvidia is arguing that the addressable AI market is expanding well beyond one buyer category.

Whilst hyperscalers may have alternative solutions now, we are looking at a bigger set of opportunity.

Campling named physical AI, sovereign AI, hyperscalers and Anthropic as parts of that wider demand picture. In this reading, Nvidia’s opportunity is tied less to the absence of competing chips in one customer segment and more to the scale and expansion of AI infrastructure demand.

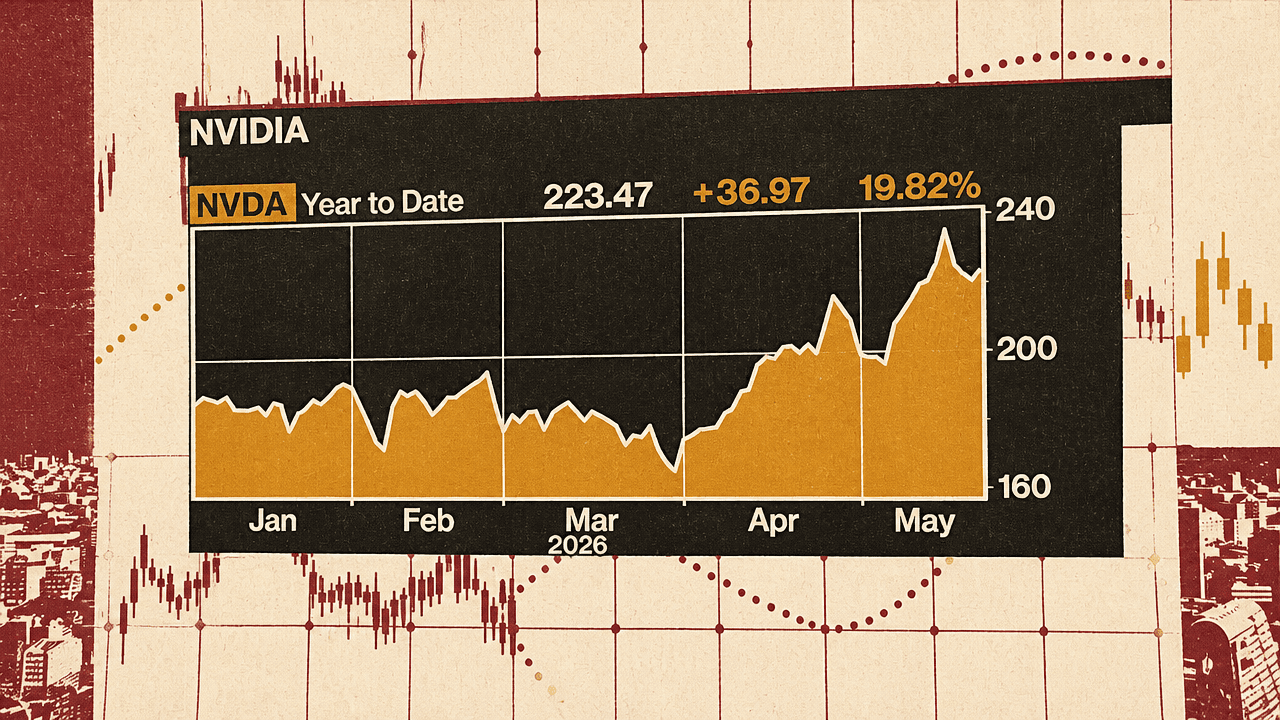

Bloomberg also displayed a year-to-date Nvidia stock chart during the discussion. The graphic showed Nvidia at 223.47, up 36.97 points, or 19.82%, year to date, with the line rising from January through May. That chart reinforced the positioning argument: Nvidia had already rallied, and the company’s strong results were being received against that prior move.

The next revenue engine is framed as infrastructure beyond cloud scale

Neil Campling said Huang had talked about AI infrastructure spending reaching as much as $3 trillion to $4 trillion a year by the end of the decade. In that framing, hyperscalers remain important, but they are not the whole revenue map. Nvidia is also pointing investors toward demand beyond the largest cloud buyers; in Campling’s remarks, the clearest named government-linked category was sovereign AI.

The Anthropic example made the speed of demand feel less theoretical. Campling referred to a Bloomberg exclusive overnight on Anthropic’s growth and described the company as moving from “no product” to $10 billion of quarterly revenue in less than three years. He treated that as evidence of the scale and speed of the AI growth set rather than as a narrow company anecdote.

His conclusion was direct: there is “no end” to the AI growth set, and Nvidia “sits at the heart of that.” The claim is not that competition has disappeared. It is that Nvidia’s market may be widening quickly enough that alternative hyperscaler chip solutions are only one part of the investment question.