Nvidia Is Moving Into the Markets Its Rivals Need

Ross Gerber, co-founder and CEO of Gerber Kawasaki, told Bloomberg that Nvidia’s rivals may be misreading the competitive threat in AI chips. His argument was that Nvidia is not merely defending its data-center GPU franchise, but moving into adjacent markets such as CPUs, edge computing and AI infrastructure for sovereign, enterprise and robotics customers, making competitors more vulnerable to Nvidia than Nvidia is to them.

Gerber’s warning runs outward from Nvidia, not inward from its rivals

Ross Gerber argued that Nvidia’s competitive problem is being misread if the focus is only on rivals trying to take share from the company’s current AI-chip franchise. His sharper claim was the reverse: Nvidia is moving into adjacent markets quickly enough that competitors should be more worried about Nvidia than Nvidia should be about them.

The competitors should be more scared of Nvidia than Nvidia needs to be scared of them because they're very good at what they do.

The backdrop for that warning was a broader technology cycle Gerber framed around the convergence of AI, space, data, and connectivity. Asked by Ed Ludlow which recent disclosures mattered most — OpenAI and Anthropic fundamentals, Nvidia’s report, or SpaceX’s long-awaited S-1 — Gerber said Ludlow had named “everything that’s important” to him in one thought.

Gerber placed SpaceX and Nvidia on different sides of the same convergence. SpaceX, he said, is helping lead the intersection of space and connectivity; Nvidia is positioned to profit from the hardware demands created by AI systems and data centers. He called SpaceX’s S-1 “one of the more interesting documents” he had read for a company in his lifetime, and described the company as highly aspirational. Nvidia, by contrast, was presented as the company already sitting in the “sweet spot” of investment flowing into AI infrastructure.

His distinction from the dot-com era was explicit. Gerber said the current period “almost feels very different than dot-com” because the companies involved are, in his view, “so legitimate,” whereas much of the dot-com boom was “BS.”

Nvidia is trying to show it will not remain just a data-center chip vendor

Ed Ludlow pressed on a detail from Nvidia’s report that he said “really jumped out”: the company’s decision, as he described it, to break out both data center revenue and edge computing revenue as separate line items. He noted that edge computing is still “a tiny part” of Nvidia’s business — less than 10% of revenue — but said Nvidia’s leadership, including Colette Kress, presented it as where “the puck is moving.”

The question was whether Nvidia could remain central to the next phase of AI computing in the way it has been central to large-language-model data center buildout. Ludlow described Nvidia’s view as an extension of its current position: even as more AI work moves toward the edge, Nvidia still intends to sit at the center.

Ross Gerber read the revenue breakout as a strategic signal. Nvidia, he said, was trying to show that it is “evolving as a business” rather than “sitting on their laurels,” collecting money from current chips, and waiting for competitors to take share. In his view, the company is moving rapidly into adjacent territory, including the CPU space, where he referred to a “hot discussion” around whether Intel might become competitive again.

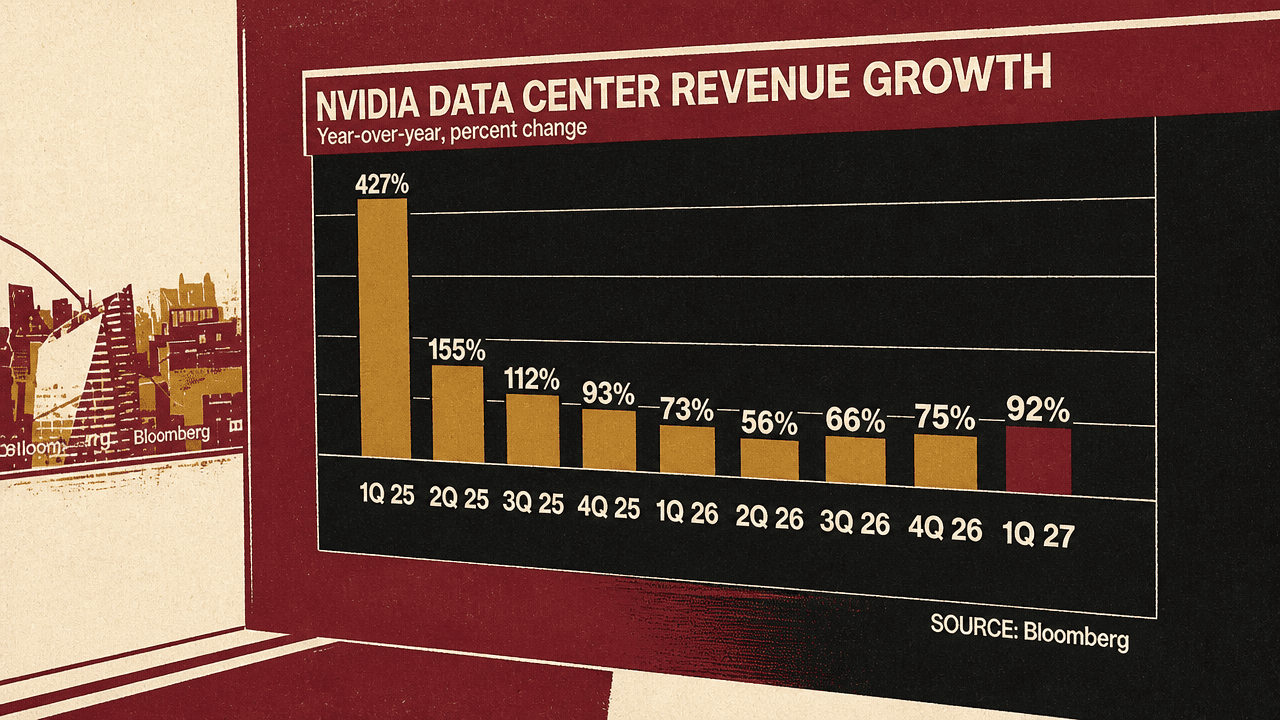

The Bloomberg chart shown during this portion showed Nvidia data center revenue growth remaining elevated even after the earliest displayed surge. The chart listed year-over-year growth of 427% in Q1 2025, falling through the middle of the period and then rising again to 92% in Q1 2027.

| Quarter | Nvidia data center revenue growth, year over year |

|---|---|

| 1Q 2025 | 427% |

| 2Q 2025 | 155% |

| 3Q 2025 | 112% |

| 4Q 2025 | 93% |

| 1Q 2026 | 73% |

| 2Q 2026 | 56% |

| 3Q 2026 | 66% |

| 4Q 2026 | 75% |

| 1Q 2027 | 92% |

Gerber’s point was that Nvidia is acting like a company that understands where attacks could come from and is already moving into places competitors might otherwise use to pressure it.

The revenue breakout points to demand beyond hyperscalers

Ross Gerber also focused on what he described as Nvidia’s breakout of data center revenue from hyperscalers versus other AI builders, including sovereign AI and robotics. In his reading, Nvidia was effectively saying it had already “made a lot of money off the Microsofts and such,” but expected to make “a lot more money in the future” as many different enterprises and governments build their own AI systems.

Gerber contrasted those systems with “open systems like ChatGPT.” The demand he emphasized was not only from the large cloud companies that powered the first wave of data-center spending, but from enterprises, governments, sovereign AI projects, robotics, and other AI builders.

A second on-screen table showed Nvidia fiscal 1Q 2027 segment revenue versus estimates. Compute was the largest line item by far. Networking and edge computing were shown ahead of estimates, while compute was slightly below.

| Segment | Fiscal 1Q 2027 revenue | Actual vs. estimate |

|---|---|---|

| Compute | $60.4B | -1.1% |

| Networking | $14.8B | +16.1% |

| Edge computing | $6.4B | +13.1%* |

| Total | $81.6B | +11.4% |

The asterisk on the displayed edge-computing figure identified it as an aggregate of estimates for other business lines. Ludlow had already emphasized that edge computing remained less than 10% of revenue, but the table showed why he raised it: the discussion around Nvidia’s position was moving beyond the core data-center compute engine.

Gerber’s warning to competitors was broader than a defense of Nvidia’s existing GPU position. He described Nvidia as pushing into CPUs, highlighting edge computing, and positioning itself for AI systems built by sovereign customers, robotics developers, enterprises, and governments.