Amazon’s AI Buildout Pushes Borrowing Higher as Capex Bill Swells

Amazon’s plan to raise at least $25 billion in a U.S. bond sale is less a one-off financing move than another sign of how large its AI infrastructure spending may become, according to Bloomberg Intelligence analyst Robert Schiffman. Speaking with Bloomberg’s Ed Ludlow, Schiffman argued that Amazon’s borrowing is scaling because capital expenditure needs are rising faster than near-term cash inflows, even as the company still has low leverage, strong cash generation and access to cheap credit.

Amazon’s bond sale points to a much larger capex bill

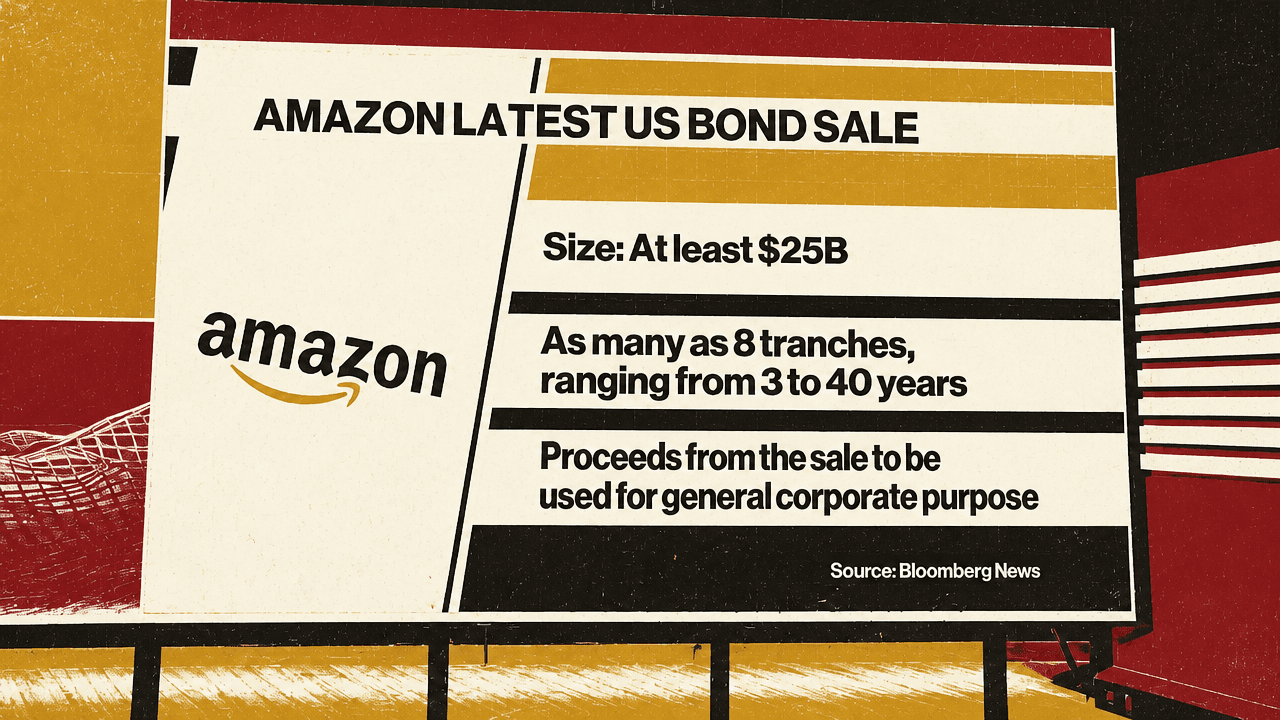

Amazon is seeking to raise at least $25 billion in a U.S. dollar bond sale, with the offering potentially growing larger depending on investor demand. The debt is being marketed in as many as eight tranches, ranging from three to 40 years, with proceeds designated for general corporate purposes.

Bloomberg reported that the possible uses include debt repayment, acquisitions, and capital expenditures. An Amazon spokesperson said the company regularly evaluates its operating plan and makes financing decisions accordingly, and that proceeds may support business investments, future capital expenditures, and upcoming debt maturities.

The financing sits inside a much larger AI-infrastructure buildout. Bloomberg Intelligence’s Robert Schiffman said Amazon’s current guidance is for $100 billion of capital expenditures in 2024, but that figure is likely to move higher as data-center infrastructure becomes more expensive. Bloomberg Intelligence framed the possible path more sharply: capex has “the potential to soar toward $300 billion next year as demand continues to far outstrip supply.”

That is the core point of the debt sale in Schiffman’s view. The $25 billion headline is not, by itself, the constraint. He told Ed Ludlow that “25 billion, it’s not that big of a number,” before adding that the deal is “getting bigger” and will probably exceed that amount. His explanation was that Amazon has already raised almost $70 billion across currencies this year, while its cash balance is above $150 billion. To Schiffman, those numbers imply that spending is rising materially rather than that Amazon is simply optimizing its balance sheet.

| Measure | Figure | Why it matters |

|---|---|---|

| Latest U.S. bond sale | At least $25B | The deal may expand depending on investor demand |

| Bond tranches | As many as 8, from 3 to 40 years | Amazon is borrowing across a wide maturity range |

| Capital expenditure guidance | $100B for 2024 | Bloomberg Intelligence says the guidance is likely headed higher |

| Possible capex path next year | Toward $300B | Schiffman ties the path to data-center costs and AI demand outstripping supply |

| Debt raised this year | Almost $70B across currencies | Schiffman’s evidence that borrowing has already scaled up |

The AI buildout is being pulled forward before the revenue arrives

Ludlow framed the financing problem as a timing mismatch. Capital expenditure growth can outpace revenue growth because the asset being built does not generate revenue until it is deployed. A data center consumes capital before it runs workloads; only after workloads arrive can it support cloud or AI revenue. He also noted that capex can rise because the same projects become more expensive, citing construction labor inflation and memory price inflation as examples discussed on the program.

Robert Schiffman agreed that multiple forces are pushing the spending number higher. First, the cost of what Amazon is buying is increasing. Second, the volume of what Amazon needs to buy is also increasing. Third, Amazon is trying to frontload as much of that spending as it can. Schiffman also said Amazon is making investments in others “like OpenAI and Anthropic” and is “feeding the ecosystem,” similar to what Nvidia is doing.

That combination makes the debt sale less an isolated financing event than part of a broader attempt, in Schiffman’s analysis, to secure capacity while Amazon currently has access to low-cost capital and is using it aggressively. He said the numbers should not surprise investors and that they are likely to “keep getting bigger and bigger.”

The amount of spending that you’re going to see over the next couple of years is going to far exceed the amount of cash that’s coming in.

The consequence is that investors will keep asking whether the AI buildout will ever generate an adequate return. Schiffman’s answer was not that monetization will quickly settle the question. Even if Amazon posts very strong cloud numbers or shows AI monetization, he said, the revenue contribution may still be nowhere near the scale of capital spending on a relative basis.

That is why he described patience as necessary but not natural. In his words, investors “need to be patient,” even though neither the bond market nor the stock market has historically been patient. The financing strategy depends on a period in which reported growth and monetization signals are visible enough to sustain confidence, while capital spending remains far larger than the near-term revenue attached to it.

The bond market has to stay open, and rating agencies have to stay unconcerned

Robert Schiffman laid out three conditions Amazon needs to manage through this phase.

The first is that the bond market has to hold up. Yields cannot “go through the roof,” because Amazon needs continued access to cheap, low-cost capital. Schiffman said Amazon currently has that access and is taking down as much of it as it can.

The second is that Amazon has to keep showing monetization, particularly strong double-digit growth across AI and cloud businesses. This does not mean the revenue immediately matches the spending. Schiffman’s point was narrower: Amazon has to keep producing enough evidence of growth to support the case that the spending is attached to future demand.

The third condition is maintaining the confidence of rating agencies. Schiffman phrased the task bluntly: Amazon needs to “continue to convince the rating agencies that none of this matters.” So far, he said, it has not mattered.

That rating-agency tolerance rests on Amazon’s leverage profile. Asked by Ed Ludlow why Amazon is the “crème de la crème” of issuers, Schiffman said that despite all the debt Amazon has issued, leverage remains very low. It is still well below the two-and-a-half-times target he attributed to the rating agencies. That gives Amazon room to borrow more.

The other support is cash generation from Amazon’s established businesses. Schiffman said the company produces substantial cash flow from its other core profitable operations. He also said Amazon can “help finance long-term growth with short-term borrowing,” a point he made as part of explaining why the company remains an unusually strong issuer despite the amount of debt it has already raised. In that framing, Amazon’s advantage in the AI debt boom is not that the AI economics are already proven at the scale of the investment. It is that the company can borrow heavily while still appearing underlevered, keep liquidity high, and use existing cash-generating businesses to carry the infrastructure buildout until the workloads arrive.